Share this blog:

In this year end report teaser of Bitcoin's Next Frontier, we take a deep dive analysis and provide key insights into the institutional demand of options and futures trading!

This Q1 2024 report is collectively written by Greg Magadini, Director of Derivatives, Amberdata; Fabio Bassani, Analyst, Amberdata; Tony Stewart, Strategic Advisor, Amberdata; Euan Sinclair, Strategic Advisor, Amberdata; and Samneet Chapel, Quantitative Researcher, LedgerPrime.

Forward

Each cryptocurrency bull market differs from its predecessors. In 2023, there is a notable emphasis on venue consolidation, particularly post-FTX, resulting in a more robust foundation.

Cryptocurrency options have gained increasing attention. Deribit, for instance, has achieved new notional open interest highs. Regulated platforms like CME also boast futures open interest surpassing any Centralized Finance (CeFi) venue, an unprecedented achievement.

These trends indicate both new market entrants and additional sources of market participation.

Amberdata, as a leader in cryptocurrency derivatives analytics, is dedicated to providing actionable insights, valuable analytical tools, and research to facilitate quick comprehension of established market phenomena.

Our commitment is to assist our customers in achieving success in these markets. Amberdata Derivatives is created by professional traders for professional traders.

INTRODUCTION

In 2023, Bitcoin once again demonstrated its resilience as an investable asset. It outperformed other major asset classes with an impressive return of over +250%. What sets Bitcoin apart is that it achieved a significant portion of this return precisely during periods of high volatility in other assets.

The SVB banking crisis in March 2023 proved to be a challenging time for stocks, leading to a roughly -4% drop in equity indexes from March 6th to March 17th. During the same period, Bitcoin surged by nearly +20%. Bitcoin’s ability to outperform not only stocks but also Ethereum and other cryptocurrencies became a defining feature throughout the year.

This exceptional outperformance was evident once more when Bitcoin responded positively to the October terrorist attacks in Israel. Much like gold, Bitcoin found its footing and surged in response to a turbulent geopolitical situation, a behavior consistent with previous instances, such as the Russian attack on Ukraine.

These situations highlight the intriguing investment opportunities that Bitcoin presents. Beyond these scenarios, Bitcoin has proven itself to be a non-correlated asset with a positive expected value, making it an ideal addition to a well-diversified portfolio.

In 2023, we witnessed the end of the Bitcoin bear market and the potential for a substantial influx of institutional capital into the Bitcoin ecosystem as the SEC considers the approval of a spot Bitcoin ETF. This investment vehicle offers traditional institutions an opportunity to invest in Bitcoin using existing “on- ramps,” such as traditional brokerage firms, without the complexities associated with Bitcoin custody.

While CME futures and related products like BITO and closed-end funds like GBTC exist, they often introduce price deviations from the Bitcoin spot price. A straightforward investment-grade product like a spot Bitcoin ETF would enable financial advisors, pension funds, and various institutions to allocate capital to Bitcoin as part of a diversified portfolio.

Considering that North American fiduciaries alone manage around $53 trillion in assets, a mere two percent allocation to Bitcoin would have a significant impact on the $858 billion Bitcoin market.

Finally, the most exciting aspect of a spot Bitcoin ETF lies in its potential to significantly expand the nascent crypto volatility market. Currently, Deribit’s notional option open interest is approximately $16 billion, which is just 2% of the underlying Bitcoin market capitalization. In contrast, the popular S&P 500 equity ETF SPY, has an outstanding notional option open interest of $880 billion, surpassing its underlying ETF NAV of $437 billion by 200%. This illustrates the substantial growth potential for the volatility trading industry with the introduction of a spot Bitcoin ETF.

DELTA-ONE

In the realm of delta-one instruments, 2023 has witnessed an intriguing divergence between Centralized Finance (CeFi) and Traditional Finance (TradFi) venues following the collapse of FTX. Typically, the cryptocurrency landscape is divided into three distinct categories: CeFi, TradFi, and DeFi.

DeFi venues primarily attract dedicated cryptocurrency enthusiasts, often comprising a

retail audience that prioritizes crypto ethos over merely trading PnL. While a handful of adventurous institutional firms have started building infrastructure to serve the DeFi space, recognizing the opportunities presented by wider spreads and less liquid markets, the majority of traditional institutional investors find the setup costs too high and the trading volumes too low to justify allocating capital to DeFi platforms.

CeFi serves as the intermediary bridge between cryptocurrency natives and professional institutions. Robust platforms like Deribit offer a seamless trading experience, featuring a variety of instruments, including conventional European cash-settled options and innovative offerings like perpetual swaps.

Lastly, TradFi solutions, exemplified by CME’s introduction of cash-settled BTC futures and options, have paved the way for conservative institutions seeking highly regulated and reputable venues to invest in the Bitcoin asset class.

THE CME PREMIUM

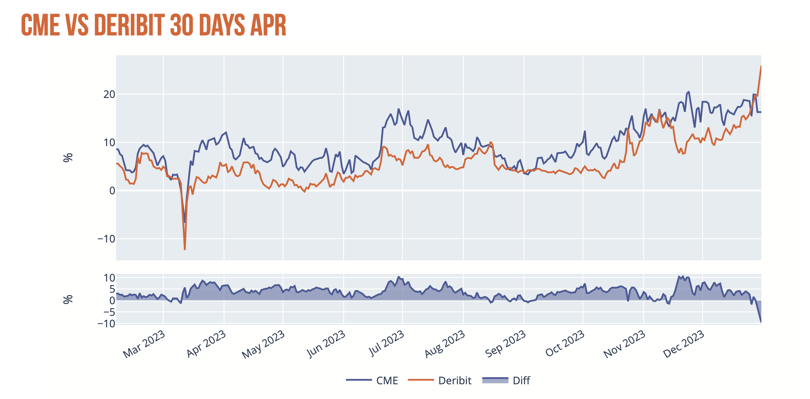

The Amberdata team has meticulously curated and structured CME data to calculate the constant 30-day rolling basis between CME futures and the Bitcoin spot market. We have also generated the same 30-day basis dataset for Deribit, enabling us to compare CME’s activity with that of another venues offering both futures and options products.

It is evident that while CME and Deribit exhibit a closely correlated trajectory for the 30-day Bitcoin futures basis, the CME basis consistently maintains a 4% annualized premium over the Deribit basis.

This data reveals two significant trends in Bitcoin investments during 2023:

Firstly, platforms like CME, characterized by stringent regulation, provide investors with a familiar and secure experience that newer venues, such as Deribit (despite their strong reputation), cannot yet match.

Secondly, 2023 is marked by a surge in institutional demand led by North American entities. U.S. institutions are willing to pay a premium for

Bitcoin exposure on CME to circumvent custody complexities and leverage existing on-ramps offered by their prime brokers.

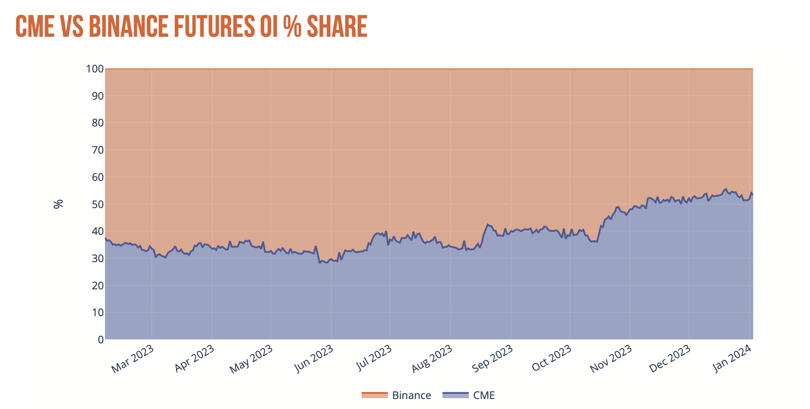

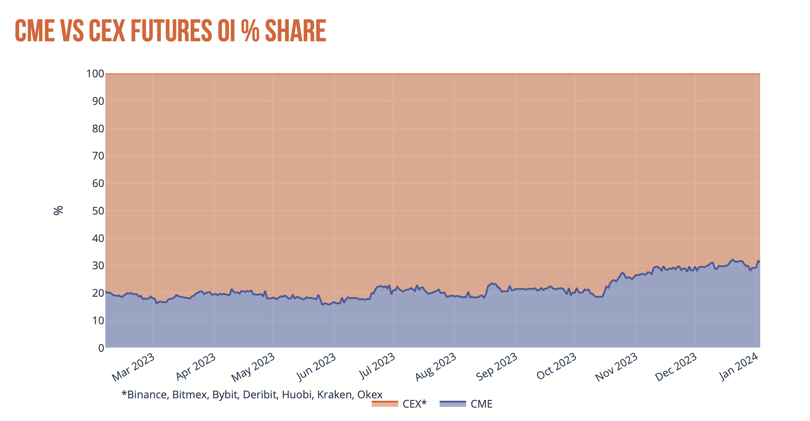

We can arrive at the same conclusion when examining the total open interest in CME Bitcoin futures. In mid-October, as Bitcoin experienced a rally, the open interest on CME surpassed that of all other delta-one venues, including Binance.

Historically, Binance has hosted the largest share of Bitcoin open interest in delta-one products like futures and perpetual swaps. However, today, CME has emerged as the largest venue. This is particularly noteworthy because Binance’s customer base differs significantly from the traditional clientele of CME and would find it challenging to transition seamlessly.

In essence, this surge in activity indicates a substantial demand for Bitcoin exposure among institutional investors, and an unprecedented development in the market.

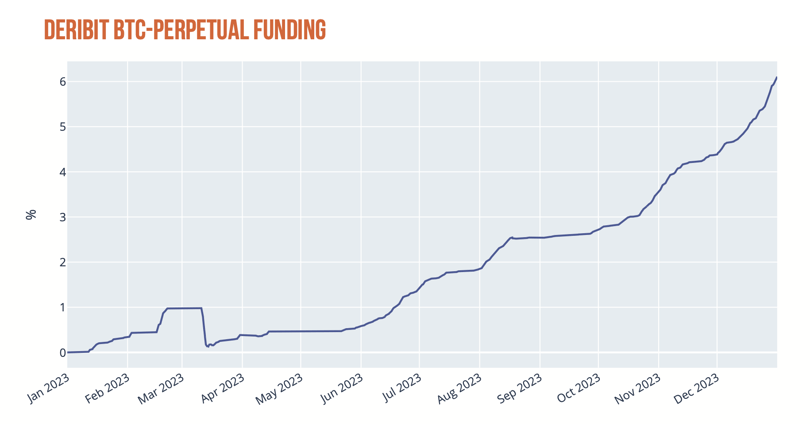

FUNDING

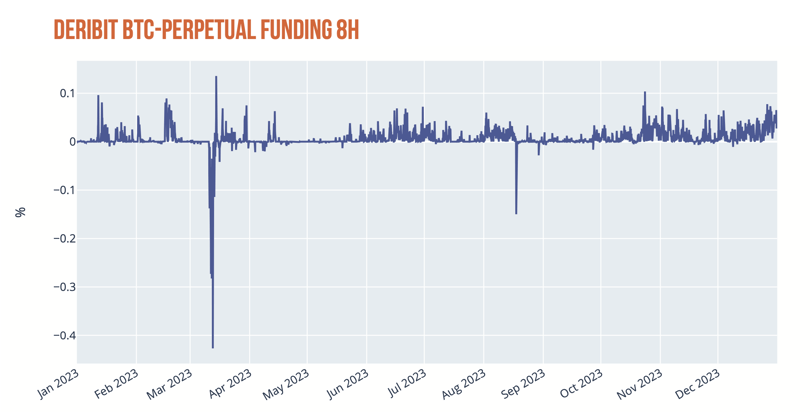

Bitmex pioneered a novel instrument in the cryptocurrency domain known as the Perpetual-Swap. Within the Centralized Finance (CeFi) venue, the most actively traded instrument is this innovative “Perp,” where funding is regularly distributed between long and short position holders. While it’s straightforward to obtain the next funding period from the platform, it can be somewhat perplexing to contrast a series of funding payments (as shown in the chart above) with the cumulative funding costs of a position. Comparing the accumulated realized funding payment stream (as depicted in the chart below) might offer a more accessible perspective.

Apart from being the most liquid instrument, the funding mechanism associated with a perpetual-swap allows traders to effectively take on a “floating” rate for the swap funding, in contrast to the relatively fixed rate inherent in a futures position.

We can observe that the cumulative funding for a long BTC perpetual position on Deribit amounted to approximately 6% in total.

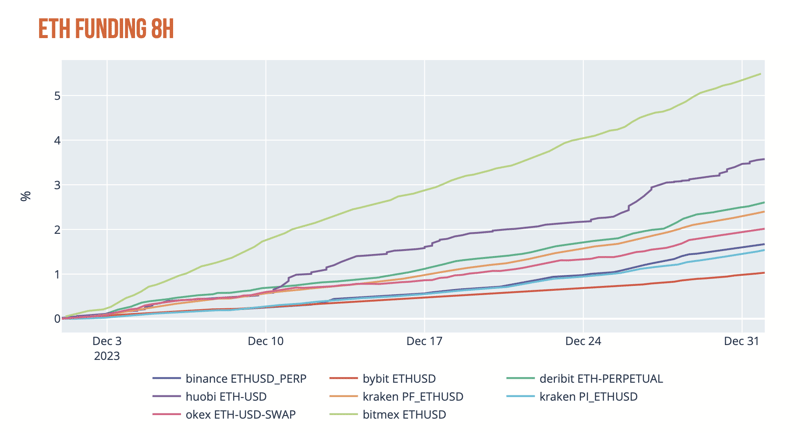

EXCHANGE DIVERGENCE

Comparing perpetual-swap instruments across various venues can yield valuable insights. In theory, all venues should have nearly identical funding costs, with only minor short-term variations based on trading flows. However, reality doesn’t always align with this expectation.

If a venue carries hidden counterparty risks or imposes restrictions on account withdrawals, significant price discrepancies and funding disparities can emerge between that venue and its counterparts.

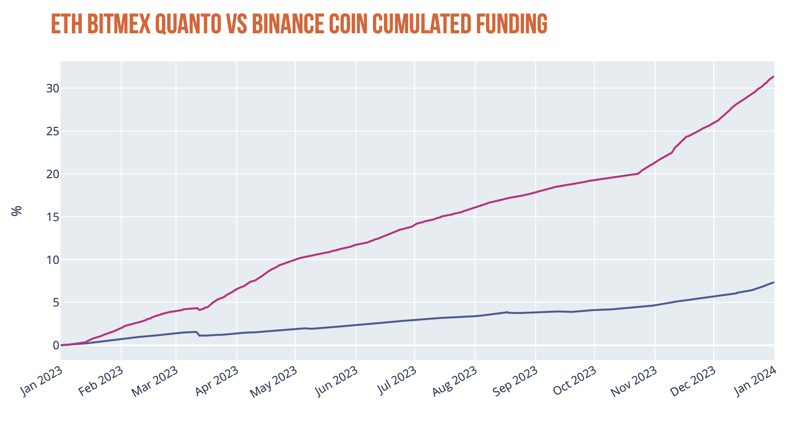

Another factor contributing to funding divergence lies within the nuances of the instrument itself. For instance, while the funding for BTC perpetuals on Bitmex closely aligns with its peers, the funding for ETH-USD perpetuals differs significantly.

This discrepancy can be attributed to the nature of the Bitmex Quanto contract, where an ETH-USD perpetual’s profit and loss (PnL) payout is denominated in Bitcoin. This setup introduces embedded convexity in the USD PnL, a feature absent in regular perpetual- swap contracts. This premium reflects a “convexity adjustment” influenced by the correlation and volatility between Bitcoin and Ethereum.

Traders can observe that the cumulative funding for the Bitmex Quanto contract amounted to 31% in 2023, in contrast to the 7% for the Binance perpetual, resulting in a substantial 24% premium associated with the “convexity adjustment.”

This premium allows traders to assess and trade the embedded assumptions within this particular type of instrument.

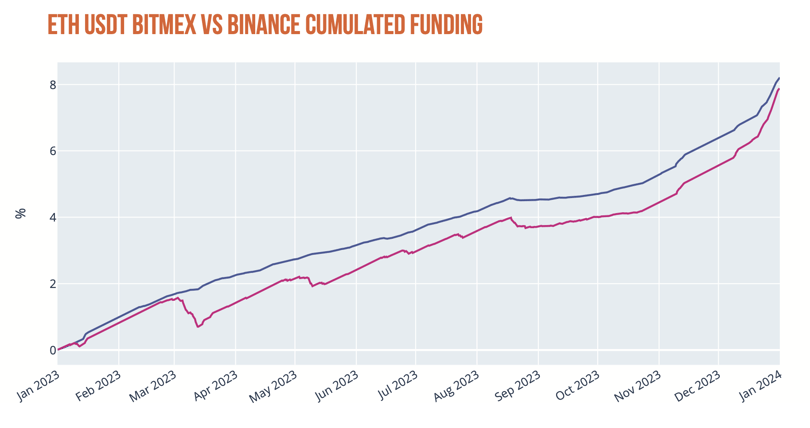

For comparison, the ETH-USDT perpetual (a stable coin denominated PnL) on both venues showed nearly identical funding rates. This eliminates the possibility that funding disparities were caused by factors other than the “Convexity adjustment.”

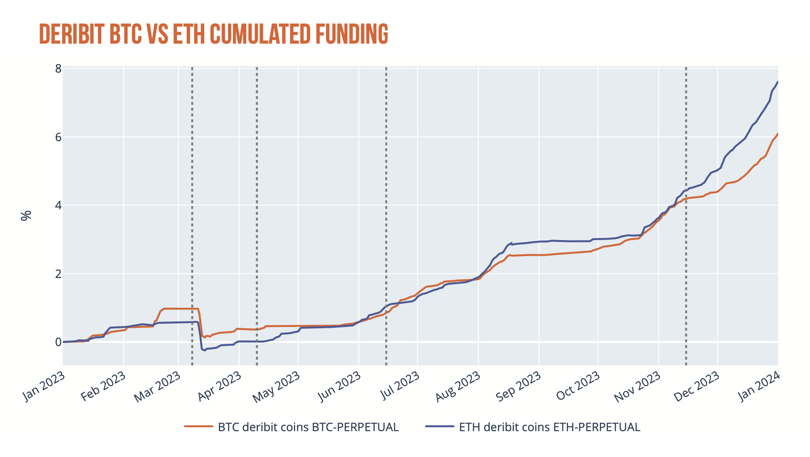

COIN DIVERGENCE

Comparing the cumulative funding among perpetual-swap instruments for different cryptocurrencies, such as BTC and ETH, can offer intriguing insights.

At the beginning of the year, Bitcoin responded positively to perceived dovishness in the US macro interest rate environment in early 2023.

In early March, following the SVB banking crisis, Bitcoin rallied significantly, outperforming Ethereum. This surge generated a sustained demand for long Bitcoin exposure, resulting in an accumulated funding premium for Bitcoin over Ethereum.

This premium gradually narrowed as Bitcoin’s volatility waned during the summer months. It’s also likely that Ethereum covered call sellers created demand for long Ethereum perpetuals as a delta hedge to their short option positions on Deribit (in terms of margin management).

Finally, in mid-November, BlackRock’s announcement of plans to file for a spot Ethereum ETF sparked increased activity in Ethereum long positions. This drove up spot prices, heightened volatility, and ultimately caused Ethereum funding rates to surge, ending the year with a +1.5% funding premium over Bitcoin perpetuals.

To continue reading the full report, click here.