Share this blog:

USA Week Ahead:

-

Monday - Markets Closed MLK

-

Tuesday 11a ET - Fed Gov. Christopher Waller speaks

-

Wednesday 2pm ET - Beige Book & Various Fed Speakers

-

Thursday - Fed Speakers throughout

-

Friday - Fed Speakers throughout

Disclaimer: Nothing here is trading advice or solicitation. This is for educational purposes only.

Authors have holdings in BTC, ETH, and Lyra and may change their holdings anytime.

![]()

CRYPTO OPTIONS MACRO THEMES:

BTC: $42,316 (-3.1% / 7-day)

ETH :$2,505 (+1.3% / 7-day)

Last week we witnessed three significant volatility events:

-

The SEC Twitter hack and fake approval.

-

The actual SEC ETF approval.

-

The commencement of the Bitcoin ETF trading.

Chart: Highlights from @Gravity5ucks via Amberdata Streamlit tool

After receiving the 'fake approval,' the most intriguing observation was the absence of an immediate news-driven reaction. This subdued response in the spot market activity was a clear indicator. It revealed that the risk of a significant gap-up was limited and resulted in the liquidation of over-leveraged positions (refer to the liquidation chart above).

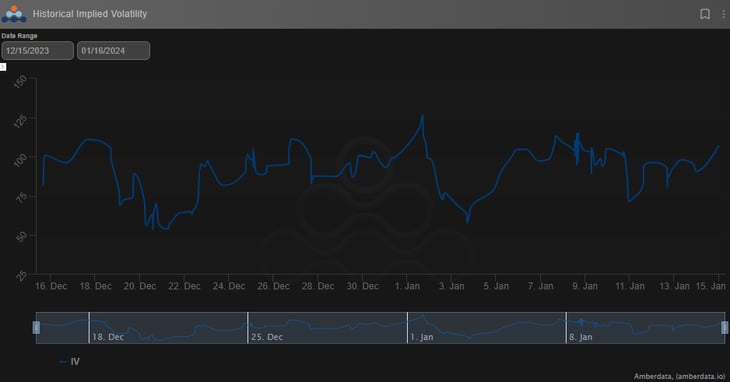

Chart: BTC ATM IV TimeSeries

The second intriguing aspect of the ETF announcement, the real one this time, was the delayed reaction in volatility selling. There was nearly an hour-long gap between the announcement and the eventual decline in implied volatility (IV) in the 7-day at-the-money (ATM) volatility.

Lastly, as we approached the first day of trading, we observed a slight increase in implied volatility leading up to the US equity market opening. However, this increase was short-lived and was followed by a subsequent decline

Chart: BTC Term Structure Richness

As Friday's US trading session began, BTC spot prices experienced a decline. This could be attributed to either a 'sell the news' sentiment or potential unlock flows resulting from the GBTC closed-end fund conversion.

Alternatively, BTC might simply be testing its trading range.

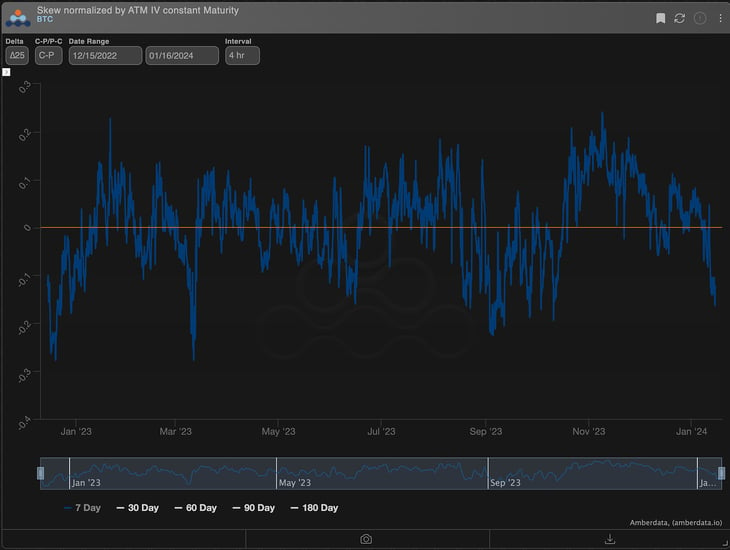

The recent downward movement in spot prices has led to the term structure moving into backwardation, while also causing the RR-Skew to approach its annual lows.

This presents a potentially opportune moment to 'buy the dip' by selling the higher front-end maturities and fading the RR-skew on the put side.

Chart: BTC 7-day RR-Skew as a % of ATM Volatility

Chart: BTC absolute IV RR-Skew for expiraitons 1/26, 2/2, 3/29, & 6/26.

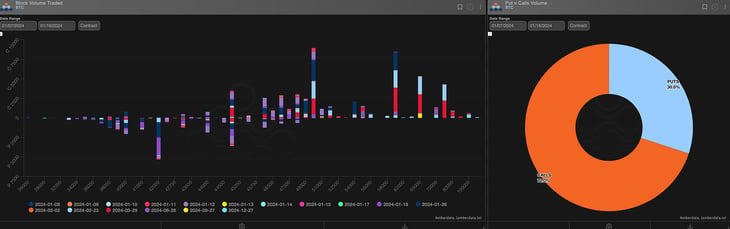

Structurally speaking, we can anticipate a larger influx of option trading activity in the wake of the BTC ETF approval.

The classic investment strategy of buying, holding, and selling covered calls, well-known in traditional finance (TradFi), is expected to become a prevalent approach in BTC volatility trading.

Moreover, well-capitalized market-makers are likely to play a crucial role in facilitating quicker responses of implied volatility (IV) in future events, as well as in managing larger option inventories.

Chart: ATM term structure: BTC & ETH

ETH has now clearly exceeded BTC in terms of implied volatility across the entire term structure. Additionally, ETH exhibits a smoother term structure curve compared to Bitcoin, likely due to the option market factoring in some volatility around the BTC halving event.

Chart: DVOL ETH/BTC rato premium/discount

When examining the historical relationships between BTC and ETH relative volatility, it becomes apparent that ETH has the potential for significantly higher implied volatility levels in comparison to BTC.

Therefore, the recent shift in volatility may indicate a return to structural norms after a counter-cyclical movement in 2023.

Paradigm's Week In Review

BTC

ETH

The Squeethcosystem Report

Crypto markets found their way lower throughout the week. ETH ended the week +9.88%, oSQTH ended the week +19.15%.

Volatility

oSQTH IV traded in a large range this week from near 100 to the low 70s.

Volume

The 7-day total volume for oSQTH via Uniswap oSQTH/ETH pool was $1.67m

January 9th saw the most volume, with a daily total of $563.89k traded.

Crab Strategy

Crab saw slight declines during the week ending at -0.33% in USDC terms.

Opyn Twitter: https://twitter.com/opyn

Opyn Discord: discord.gg/opyn

AMBERDATA DISCLAIMER: The information provided in this research is for educational purposes only and is not investment or financial advice. Please do your own research before making any investment decisions. None of the information in this report constitutes or should be relied on as a suggestion, offer, or other solicitation to engage in or refrain from engaging, in any purchase, sale, or any other investment-related activity. Cryptocurrency investments are volatile and high-risk in nature. Don't invest more than what you can afford to lose.