Share this blog:

Providing liquidity on Decentralized Exchanges (DEXs) can be a great source of passive yield for investors and allows them to hold underlying tokens while earning a portion of trading fees from swaps in a pool. Uniswap v3, currently the largest DEX on Ethereum, added another beneficial factor for liquidity providers (LPs). Liquidity providers can concentrate their trading fees from their deposited capital within custom price ranges rather than uniformly spreading liquidity across a large price curve and causing increased slippage costs. This is especially beneficial for stablecoin pools, where the variation in price from a peg is often minuscule.

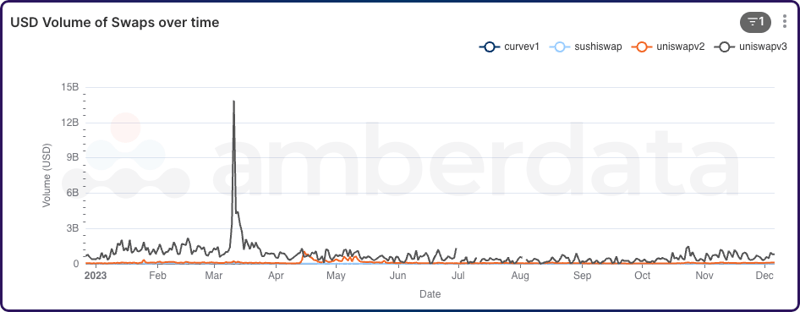

Uniswap v3 had the largest swap volume between December 2022 and December 2023

While the benefits of Uniswap v3 over v2 are clear to DEX traders, liquidity providers may be taking on more risk. Capital might not be actively used outside of their ticks in exchange for higher trading fees, so opportunity costs and exchange rate changes could mean LPs are unprofitable or are readjusting wasteful concentrated liquidity positions to avoid impermanent loss.

As we describe in our guide on impermanent loss, impermanent loss (IL) is the opportunity cost a liquidity provider faces when the net price difference between assets changes from the time they were first deposited. It is considered impermanent because liquidity providers can recover their loss if the token pair returns to the initial exchange rate.

While tracking impermanent loss is crucial for liquidity providers, it is an extremely tedious process, especially since its value may change after every action in a pool and considering that values must be normalized to a common denominator such as USD. Amberdata’s Uniswap v3 Impermanent Loss feature calculates fees, returns, and losses at the event level and takes liquidity distribution into account.

Using Amberdata’s extensive Uniswap v3 data, we will understand how prices and liquidity affect Uniswap v3 LP’s impermanent loss by comparing historical returns across three popular pools: USDC/USDT, WBTC/WETH, and PEPE/WETH. We will denote IL as a negative value, with more negative values (ex. -1) being higher losses and more unrealized capital than less negative values (ex. -0.01). Additionally, while DeFi prices are always denominated in WETH, we converted the token’s price (for example USDC) to WETH, and then from WETH to USD for improved readability. This may result in token prices that do not appear as expected.

Tracking Impermanent Loss: Price and Impermanent Loss Correlation

The USDC/USDT Pool

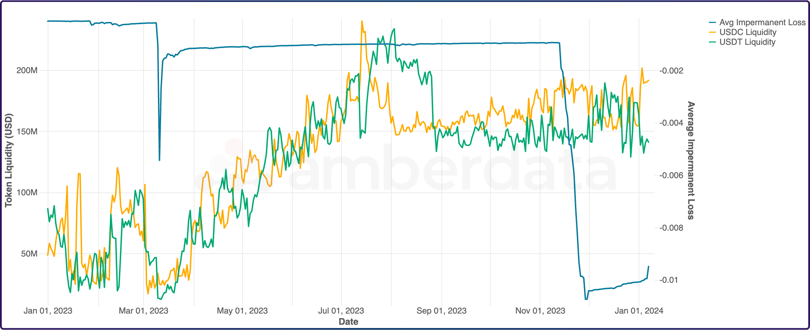

Average LP IL to pool liquidity from January 1, 2023, for USDC and USDT

Given it consists of two stablecoins, the USDC/USDT pool has generally been fairly stable in terms of liquidity and low impermanent loss. Throughout 2023, the USDC/USDT pool grew steadily to over $150 million in liquidity for each token, and the tokens’ pool liquidity remained fairly even. However, liquidity became unstable since the summer of 2023 due to pool imbalances throughout the DeFi landscape mainly caused by the Curve 3pool imbalance.

As seen above, sometime at the end of December IL went from 0.095% to 1.075% despite the overall liquidity remaining stable. The main reason for this was a huge liquidity imbalance between USDC and USDT with USDT being swapped for USDC before the imbalance swapped back along with IL moving back below -0.1%.

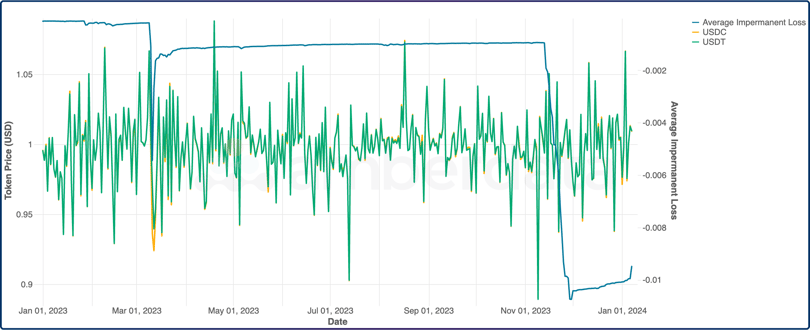

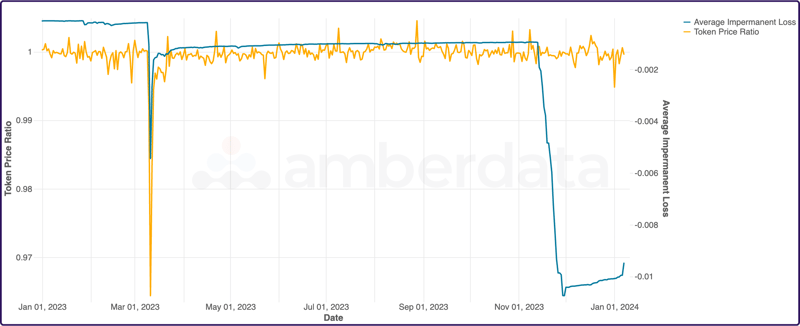

Average LP IL to token prices since January 1, 2023, for USDC/USDT

Looking at prices, the two tokens have been in lockstep throughout most of the year. Despite some minor USDC depeg events (specifically one in March after the SVB collapse), stablecoins continue to be stable.

The WBTC/WETH Pool

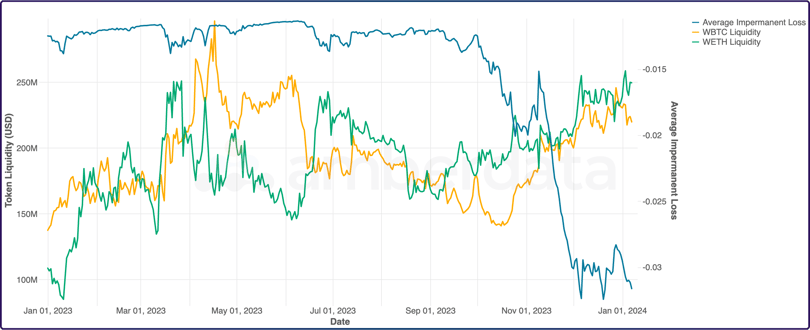

Average LP IL to pool liquidity since January 1, 2023, for WBTC/WETH

Switching to a slightly more volatile pool, the WBTC/WETH pool has had far more underlying token price volatility than stablecoin pools. Liquidity fluctuated for this pair throughout the turbulent year that was 2023.

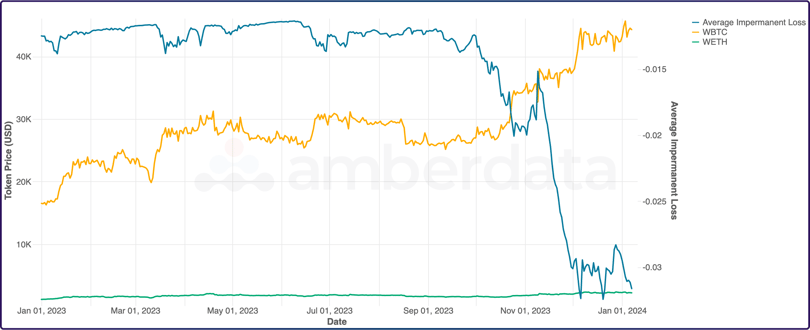

Average LP IL to token prices since January 1, 2023, for WBTC/WETH

One interesting pattern that emerged from the WBTC/WETH pool was that impermanent loss followed price variation. This makes sense: as token prices diverge, there is more demand for one token over another, which leads to IL.

While the token prices held steady throughout early 2023, IL kept pace and stayed within a small range. As the price of BTC began to skyrocket during October and continued through the end of December, IL went from around 1% to over 3%. As WBTC began to rally, WETH remained relatively flat in comparison.

The PEPE/WETH Pool

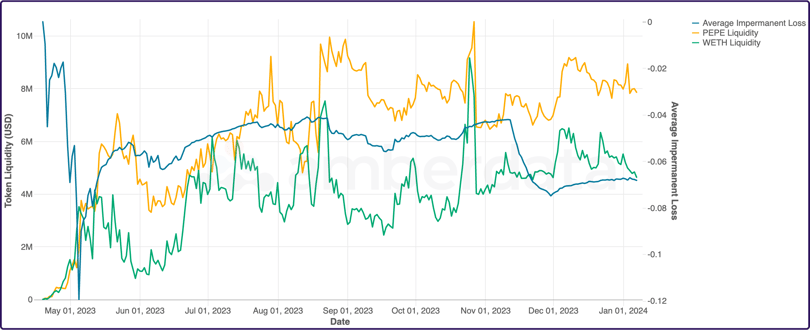

Average LP IL to pool liquidity since January 1, 2023, for PEPE/WETH

The PEPE/WETH pool represents a much more volatile market than the previous pools. This pool maintained an average IL of around 5% throughout most of the year but then saw values hit almost 8% at the end of November 2023.

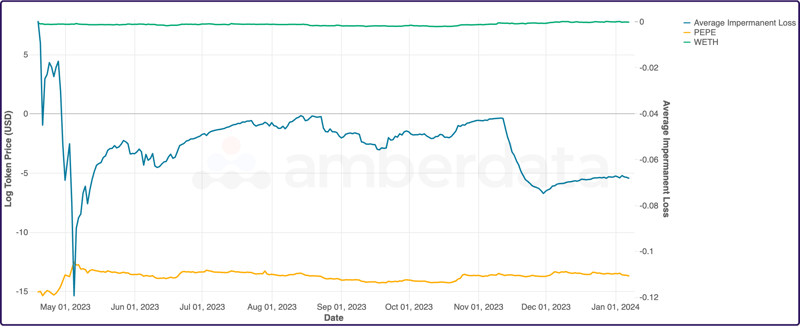

Average LP IL to log token prices since January 1, 2023, for PEPE/WETH

As WETH token price appreciated through November and December, impermanent loss moved into an almost direct correlation with price differences. A noticeable change in average IL mid-November has slightly rebounded with both PEPE and WETH prices increasing.

Managing Impermanent Loss

The previous three examples have shown how impermanent loss can be correlated with the token price ratio. Now, we will dive into several techniques for managing IL across different pools.

Mitigating Impermanent Loss Strategy #1: Rebalance Portfolios

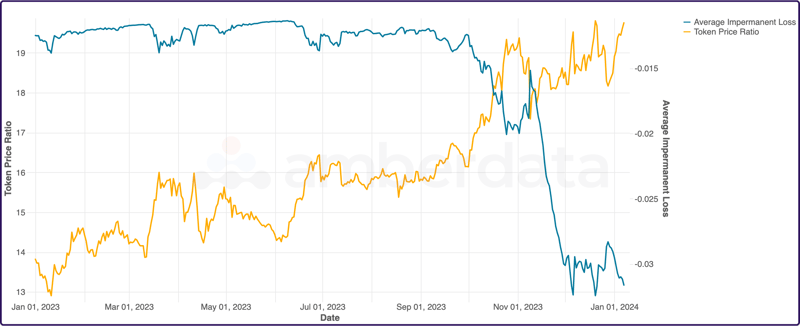

Average LP IL to token price ratio since January 1, 2023, for WBTC/WETH

First, we looked at the WBTC/WETH pool. As the token price ratio, or the price of WBTC divided by the price of WETH grew, impermanent loss became much more negative. This is likely due to the demand for WBTC outweighing the demand for WETH.

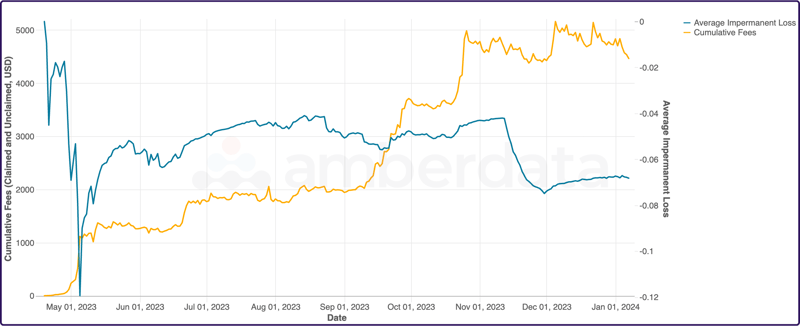

Average LP IL to cumulative holder fees generated since January 1, 2023, for WBTC/WETH

We can also see that impermanent loss was offset by cumulative fees, which grew due to the increased trading volume during October of 2023. A strong mitigation strategy to respond to impermanent loss caused by extreme price fluctuation is to rebalance portfolios.

If the price discrepancy is expected to continue, (ex. LPs are now more bullish on BTC prices than ETH prices), rebalancing can reduce the exposure to further losses. Comparing returns on Uniswap v2 and Uniswap v3 can also provide optionality within the Uniswap ecosystem. Read more about impermanent loss mitigation strategies on Uniswap v2 here.

Mitigating Impermanent Loss Strategy #2: Understand Pool and Token Behavior

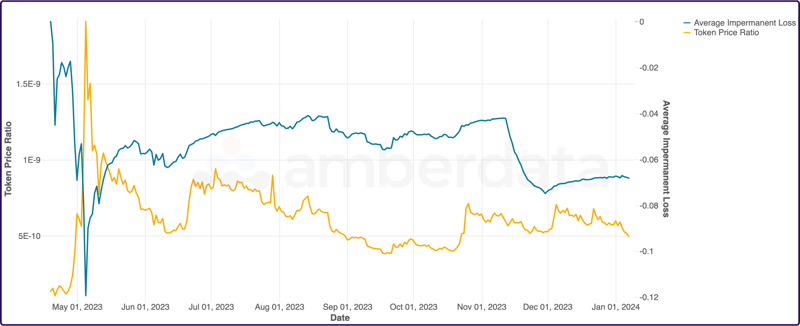

Average LP IL to token price ratio since January 1, 2023, for PEPE/WETH

For the PEPE/WETH pool, a similar pattern to the WBTC/WETH pool emerged, with IL being correlated to the average price ratio.

Average LP IL to cumulative holder fees generated since January 1, 2023, for PEPE/WETH

After looking at the cumulative fees, we can see that the impermanent loss was directly offset by fees generated from providing liquidity. As the IL grew, more fees were generated due to the higher trading volume. That is not to say there is a causation between the two. Fees are generated from pool swap volume rather than due to swap volumes for each token, but there is an expectation that if the pool behavior switched (for example, users began swapping ETH for PEPE rather than PEPE for ETH), we would see lower impermanent loss and rising fees as the trading imbalances returned to parity.

We saw this pattern in May of 2023 when PEPE was the hot token. The impermanent loss was significant when the price delta of PEPE to ETH was high. However, as the price ratio stabilized into June, IL also flattened.

Mitigating Impermanent Loss Strategy #3: Monitor for Whales

Average LP IL to token price ratio since January 1, 2023, for USDC/USDT

Unsurprisingly, the USDC/USDT pool had very little token price ratio variance but had a large change in impermanent loss at the end of November 2023. The biggest change in the token price ratio came in March 2023 during the Silicon Valley Bank crash which led to a major de-peg in USDC.

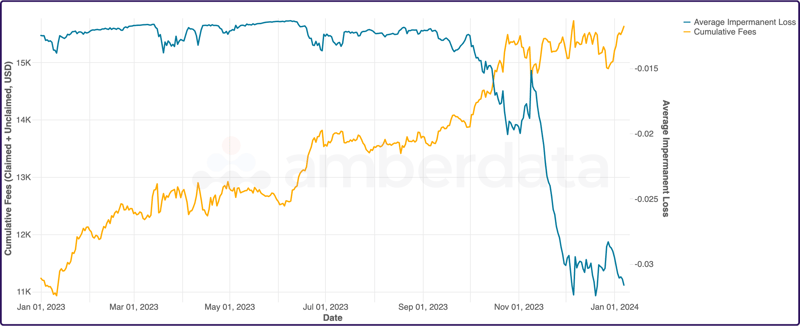

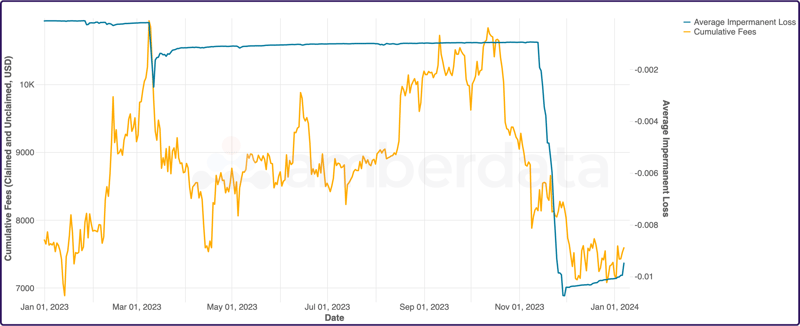

Average LP IL to cumulative holder fees generated since January 1, 2023, for USDC/USDT

This pool gives us a completely different dynamic and illustrates a pitfall of our analysis: IL grew as cumulative fees dropped. This tells us that there was a shift in positions held in the pool: likely, a whale or group of whales who had accumulated the lion's share of fees left the pool, perhaps to trade the October bull run. The best way to monitor for whales and mitigate risk is to use Amberdata’s Liquidity Provider Positions endpoints. The whale(s) also had less impermanent loss, which only exacerbated the pool’s remaining LP’s average IL.

As an LP, the change in LP structure from events such as a large whale leaving the pool will not change anyone’s IL ratios. It may benefit the remaining LPs as they can collect more fees generated from the pool. However, a whale leaving the pool can create a large pool imbalance, which can cause token price slippage and make the overall IL rise. To mitigate impermanent loss, whales and other liquidity providers’ movements within a pool should therefore be monitored extremely closely.

Conclusion

While impermanent loss on Uniswap v3 is based on individual portfolios, analyzing various scenarios within different liquidity pools helps LPs understand the mechanisms behind impermanent loss as well as their positions and risks. Because impermanent loss is very affected by timing, the frequent use of risk mitigation strategies helps LPs make more informed decisions on their positions and know when to enter and exit pools.