Share this blog:

.png)

Geopolitics is taking the driver’s seat this week, overshadowing traditional macro releases and pushing volatility across commodities and risk assets. Crypto options markets are already pricing aggressive downside, with skew and term structure reflecting heavy hedging demand. Here’s what derivatives data is signaling for short-term positioning and the medium-term outlook.

USA Week Ahead (ET):

- Wednesday 8:15 am - ADP employment report

- Friday 08:30 am - NFP Employment Report

Various Fed Governors speak throughout the week

MACRO Overview

Iran's geopolitics are going to be the main driver of oil, gold, and silver prices along with their associated volatility.

It will be interesting to see how risk assets react to developments this week.

I believe risk-assets will then drive the crypto market's direction.

There are also rumblings around private credit that seem to be dragging risk-assets lower, including AI stocks.

Last week, we had the PPI numbers come out a bit mixed. Although the overall headline number was worse than expected, +0.5% vs +0.3% expected.

This week, we have the Non-farm payrolls number and the unemployment rate being published.

Although these are important releases, especially given the recent downward revision of -900k jobs for 2025, I don’t think it matters right now, given geopolitical developments and potential impact to AI from private credit.

BTC: $67,059 (-0.5% / 7-day)

ETH: $2,021 (+3.0% / 7-day)

SOL: $86.41 (+3.2% / 7-day)

Crypto Options Overview

With all the uncertainty in the crypto markets right now, what’s the play?

There are good arguments for the longterm buy-hold position and strong opposing arguments that a bottom can’t be truly found until DATs capitulate.

To me, what seems like the best play is found in the volatility space, not the directional delta (at least for the next few weeks).

Chart: BTC spot (tradingview.com)

In my mind, the downtrend is NOT broken and we should expect more downside overall (in the medium term), but the short-term likely needs more sideways price consolidation.

What I’m seeing right now is a very “jittery” options market that has ALREADY priced in a lot of downside in price volatility… I don’t think Bitcoin put buyers are going to be rewarded well.

Chart: ∆25 RR-Skew (pro.amberdata.io)

If we look at the ∆25 risk-reversal skew (above), we see pricing is very bearish and the downside volatility hit extreme levels for short-dated options… Today it remains aggressively priced.

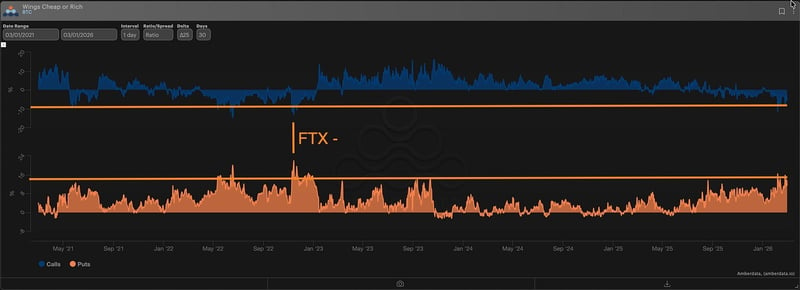

Chart: ∆25 Wings (pro.amberdata.io)

We can further decompose the ∆25 Risk-Reversal into two separate wings (the put wing and the call wing) to understand which component of the surface is driving the risk-reversal.

The put wing (30-dte, ∆25) is pricing in the same premium to ATM vol (ratio) as the November 2022 FTX crisis.

Are we REALLY there?

The call wing is also discounted to similar levels…

Part of the reason for this extreme volatility positioning is likely due to IBIT options investors bringing “TradFi” driven flows… using options to hedge their books (without taxable sales)… buy protective puts… sell covered calls.

That said, I do think today’s downside is overly dramatic for the current market.

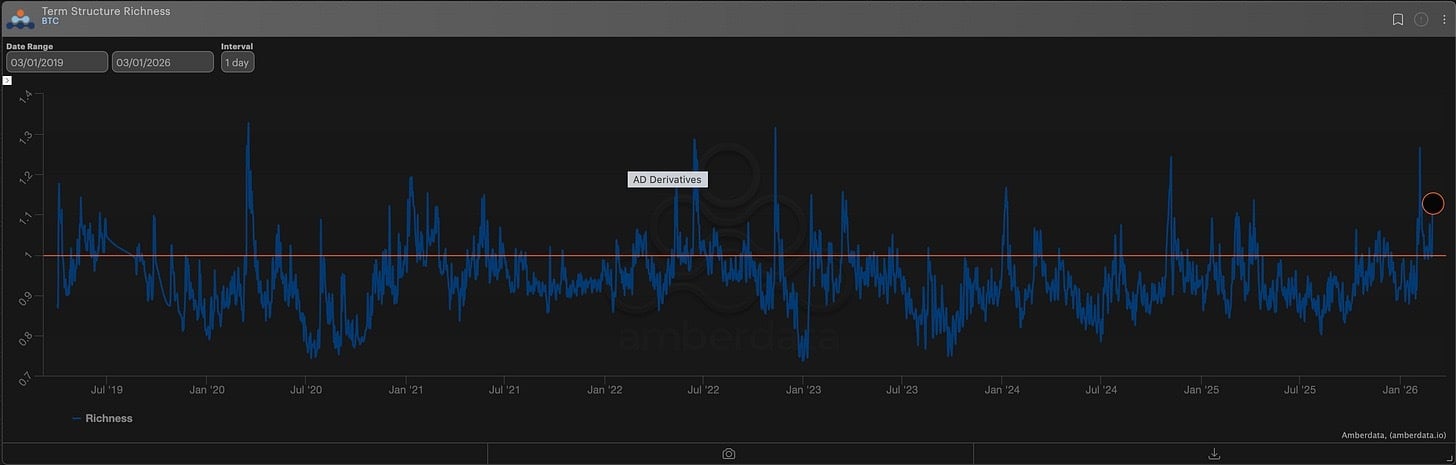

Chart: Term Structure Richness

Looking at the overall volatility premium, we can also see that current term structure backwardation is pricing in extreme levels too.

This signals that overall short-term options are carrying a LARGE premium… and within the short-term complex, puts are even MORE expensive.

Instead of “buying the dip,” providing liquidity to the put buyers seems like the trade today, for the short-term horizon.

That said, I still believe the medium-term horizon has NOT found a bottom.

Chart: ETH/BTC via TradingView

The BTC downtrend isn’t broken, but even worse is ETH. For downside exposure I like the short ETH trade.

The chart above shows the ETH/BTC ratio, which currently seems to be resuming the price downtrend since Nov 2022 FTX.

After a brief rebound in 2025 ETH looks like it’s ready to give up the gains and potentially retest the 0.02 pricing point.

AMBERDATA DISCLAIMER: The information provided in this research is for educational purposes only and is not investment or financial advice. Please do your own research before making any investment decisions. None of the information in this report constitutes, or should be relied on as a suggestion, offer, or other solicitation to engage in, or refrain from engaging, in any purchase, sale, or any other investment-related activity. Cryptocurrency investments are volatile and high risk in nature. Don’t invest more than what you can afford to lose.