Share this blog:

Bitcoin prices have been on a roller-coaster of volatility that often affects the entire cryptocurrency asset class. Futures provide leveraged price exposure to digital assets without needing to understand the underlying mechanisms and protocols. This post will be chart heavy, and try to show technical data in as simple format as possible.

Before jumping into cryptocurrency futures, its worth looking at how traditional futures work. Trading in derivatives is not new. Speculators and commercials participate in the futures markets across many assets, currencies, commodities, stock market indices even weather! Due to the specifics of different assets, there are often financing and storage costs associated with these contracts often called the cost of carry. Some market participants exploit the differences between contracts.

Basis

Basis is the difference between the contract price and spot market price.

For assets that are delivered and settled into the spot markets, this can create an opportunity to spread trade the difference between spot and futures contracts. The basis implies a cost of carry, seasonality, or other factors which impact the forward (in time) price.

Basis APR

Contract APR is effectively the annualized cost of carry implied in the forward curve across a series of futures contracts. When a market is in Contago the forward price of a futures contract is higher than the spot price. When the forward price is less than the spot the market is said to be in backwardation. When a market is in contango, yield can be generated buying the spot & selling the future

Yield can best be determined in a simple formula:

Basis = buy spot, sell future

OR

Basis = sell spot, buy future

Depending on which side the spot or contract price ends up on expiration determines the yield.

As an example of this, you can think of a commodity Wool getting traded from farm to distributor. A future contract with expiration of July is setup, where a buyer commits to buy 100 containers of Wool at a certain price, and seller sets a price they are willing to sell 100 containers. At the conclusion, a buyer and seller are matched, and the trade executes. Profit occurs for the buyer OR the seller depending on the final price and the pre-committed future price.

Take a look at the BTC Contracts on FTX. This shows the current values of contract basis & volumes for front month, back month & far month:

FTX BTC Futures Contracts

FTX BTC Futures Contracts

A few interesting things to note, the trend of future price is definitely moving significantly upward. (A metric which we’ve shown actually follows the Stock to Flow model Plan B established for Bitcoin, and is easy to use via API). Based on the Days To Expiration (DTE), it also appears that the basis APR % indicates more yield in the short term.

How does Bitmex & Huobi front month & back month contracts look?

Bitmex BTC Futures Contract

Bitmex BTC Futures Contract

Huobi BTC Futures Contract

There is a trend certainly forming here, front month contracts are indicating the highest yield.

A better way to view futures contracts, is by using an Implied Yield curve to get the full picture of an assets contracts:

FTX Implied Yield

Huobi & Bitmex Implied Yield

Huobi & Bitmex Implied Yield

These charts show both volume as well as Yield for all BTC Contracts. With a Yield Curve, you can understand the cost of carrying the asset or what the market is demanding as a premium for its risk. Market makers and exchanges may have a surplus or a shortage in their books and need to change their BTC loan rates, which would impact the yield curve.

Which contract on which exchange is performing the best?

Comparing the implied yield across each exchange shows a couple crucial factors — where the most trade volume occurs (stability) and which APR has the highest Yield (similar to arbitrage).

BTC0625, BTC0924, BTC1231 Contracts on FTX, Bitmex, Huobi

Different exchanges have higher or lower yield per-contract. After seeing this, I began to wonder what the historical performance view portrayed across exchanges and contracts…

Cross-Exchange BTC0625 Yield Performance

As you can see from this front month historical view, Huobi and FTX follow a very similar pattern but have wildly different values from Bitmex. Is Bitmex following its own patterns here? Is it just this contract? How about back month comparison:

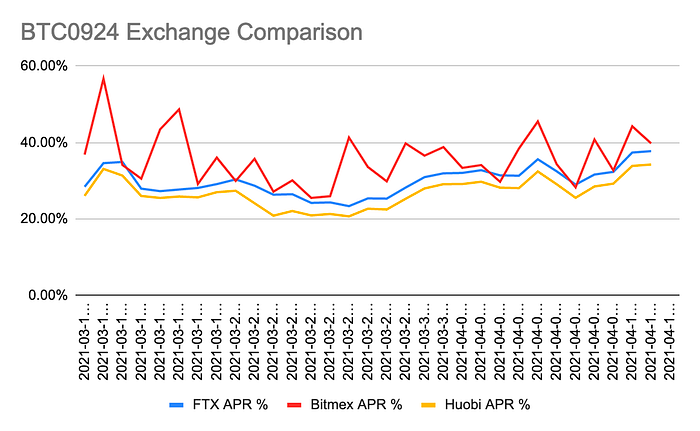

Cross-Exchange BTC0924 Yield Performance

Bitmex trendline follows almost identically, with some variance. More interesting however is the overall APR % are more tightly knit. There are even some events where the APR has crossover against FTX. It would appear that Bitmex has quite a volatile set of contracts compared to Huobi and FTX.

Which brings me to another question, how do futures perform compared to spot? (Obviously the basis is directly tied to spot/future) What does the historical trend show?

FTX Contract Comparison

Bitmex Contract Comparison

Huobi Contract Comparison

Quick thing to note here: Huobi has the lowest volume by far (not shown in these charts), so trend is still too early to draw final conclusions.

Let’s break down the charts:

-

The APR historical movements across contracts are very similar, FTX being the most stable in terms of day-to-day variance.

-

Bitmex has a front month contract that holds the most ground (over 50% of the total available implied yield)

-

FTX appears to show quite an even spread across its contracts over time

How does volatility compare against Futures & Spot?

For this, we need to look at the contract prices and spot price over time:

Huobi, Bitmex, FTX —Futures vs Spot Prices

Huobi, Bitmex, FTX —Futures vs Spot Prices

With a few exceptions, the general volatility and price fluctuations directly match the spot asset. Are futures less volatile than spot? Are there implied yields indicative of a profitable basis APR? You decide. :)

. . .

Comparison Methodology

It’s worth mentioning the sources of data used in the charts. Since Amberdata provides realtime trades, ohlcv, tickers, orderbooks and more, I needed to show comprehensive like-kind data sets. Here’s my methodology:

-

All single day comparisons and tables utilized the close of OHLCV for both spot and futures, using the futures timestamp and expiration against same spot timestamps. End of day timestamp being: “2021–04–11T00:00:00.000Z” or Midnight UTC April 11th, 2021

-

All historical comparisons utilized the close of OHLCV, again for all data points in futures and spot assets. Timestamps used: Start — “2021–03–12T00:00:00.000Z” or Midnight UTC March 12th, 2021, End — “2021–04–11T00:00:00.000Z” or Midnight UTC April 11th, 2021

. . .

Get into Crypto Futures!

All data represented in this blog is available in Amberdata.io APIs:

Thanks to Shawn Douglass.