Share this blog:

It has been an exciting two weeks for the digital asset space since our last newsletter. Let’s review some highlights:

-

ConsenSys announced the SEC is closing their investigation. After several months of legal uncertainties, Ethereum had a massive win this week after the SEC announced that they closed their investigation into ETH 2.0 as a security. If declared as a security, it would subject ETH to governance under the SEC. The SEC was quickly countered by a lawsuit from ConsenSys, a close partner of the Ethereum Foundation, who argued that ETH should be classified as a commodity instead. With the approval of ETH ETFs, it seems the SEC is backing away from this fight for now, but there remains no formal ruling on ETH as an asset class. This is one of the many legal wins the digital asset space has taken in the last few months.

-

Paxos releases USDL, a new stablecoin. Paxos launched a new USD stablecoin, issued by the UAE. US customers are blocked as users of the new stablecoin, with Paxos citing uncertain regulatory guidance. This stablecoin will offer a daily 5% rate, in line with Treasury bonds. It will be interesting to see how this stablecoin will stack up against the many other stablecoins in the digital asset space.

-

Tether launches a new gold back stablecoin, Alloy. Many have criticized the US dollar for diverging from a gold-backed dollar. With Tether’s new stablecoin, aUSDT, critics can rejoice as they have the opportunity to purchase a gold-backed dollar. With the launch of this and USDL, it is clear that stablecoins remain one of the most popular applications in the digital asset space.

-

Franklin Templeton announces USDC to USD conversion on the Benji platform. To wrap up our stablecoin news, Franklin Templeton recently announced that they would honor USDC as USD on the Benji platform. As more TradFi firms recognize the value of digital assets, more average people will have the opportunity to participate in the space.

Spot Market

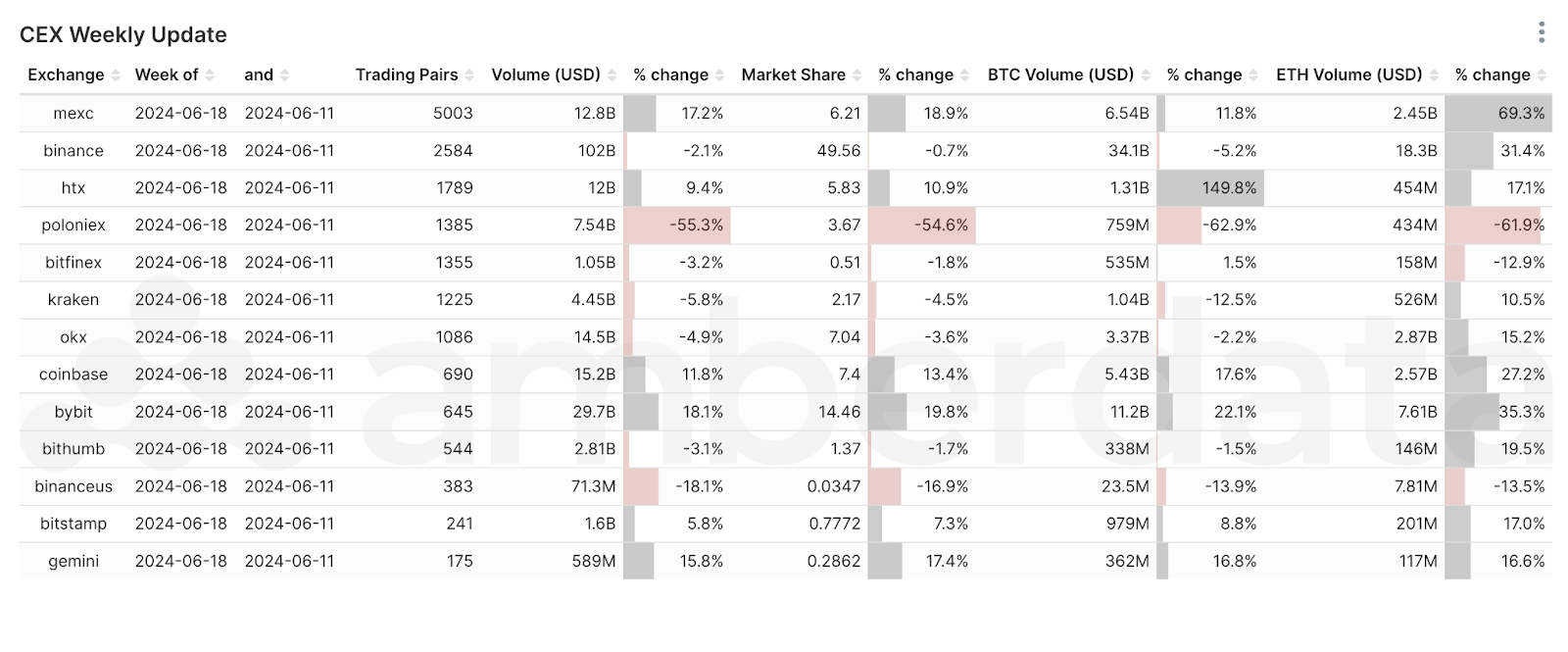

Centralized Exchange (CEX) comparisons from weeks 6/05/2024 and 6/18/2024

Spot trade volume by exchange over the past quarter

Spot trade volume remained fairly consistent throughout the past quarter, except for a sudden spike in trading volume for Poloniex on June 9th. While it’s unclear what caused the spike, Poloniex often announces delisting on their news and announcement page. It’s possible there was a surge in traffic after a large delisting was announced on June 7th.

Volume traded (USD) on CEXs over the past quarter

We can see that the volume traded on CEXs has significantly decreased over the past quarter. This is troubling, as even though BTC remains near its ATH, we are not seeing the typical corresponding activity on CEXs. This implies that retail may not be as invested in the current hype cycle as we expected. Keep an eye out on this metric: if we see a continual decrease, it could be an early warning signal that investors are starting to fold.

DeFi DEXs

Decentralized Exchange (DEX) protocol from weeks 6/05/2024 and 6/18/2024

Uniswap v3 trading volume for top pools over last quarter

As we mentioned at the beginning of the snapshot, stablecoins are arguably one of the most important applications in the digital asset landscape, and DEXs continue to validate this story. Of all pools on Uniswap V3, stablecoin to asset pools makeup nearly 90% of the trading volume. It will be interesting to watch if USDL or aUSDT can challenge USDT_WETH’s spot as the top DEX pool. You can tell a stablecoin's dominance by its overall favorability as a pool in a DEX - over the next few weeks, watch out for these new stablecoin pools, and see how the market reacts to them.

DeFi Borrow/Lend

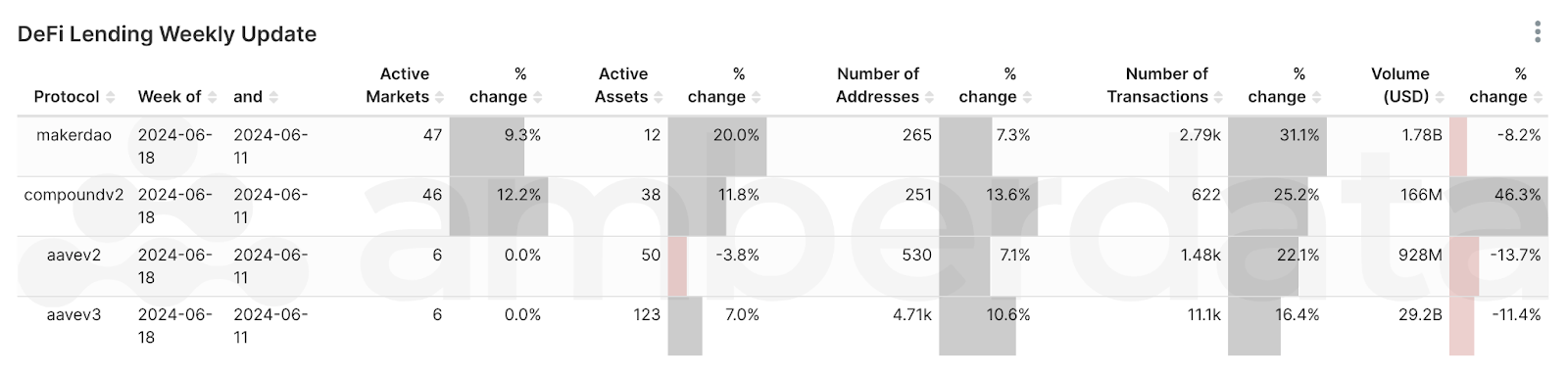

DeFi Lending protocol comparisons from weeks 6/05/2024 and 6/18/2024

DeFi Borrowed Volume by protocol and network

Borrowed volume by protocol and network is an interesting metric as it shows how popular each lending protocol is on each platform. AAVE and MakerDAO remain the clear winners of the space, taking over 80% of loan shares across all other lending protocols. Aave V3 in particular continues to grow and is up nearly 10% in borrow share from the start of the quarter. This is good news for Aave, as the lending community faces tough times in a world with stablecoin yields.

Defi Repaid Volume by Protocol and Network

Repaid volume by protocol and network in comparison tells a much different story. We see repaid volumes are much smaller daily (100s million vs billions) and the repayment distribution varies significantly by protocol. Aave V3 repayments appear pretty cyclical, whereas other protocols vary significantly from day to day. Repayment is expected to be lower, due to the nature of lending protocols, but strong deviations in repayment schedule can be an indicator of bad loans.

Networks

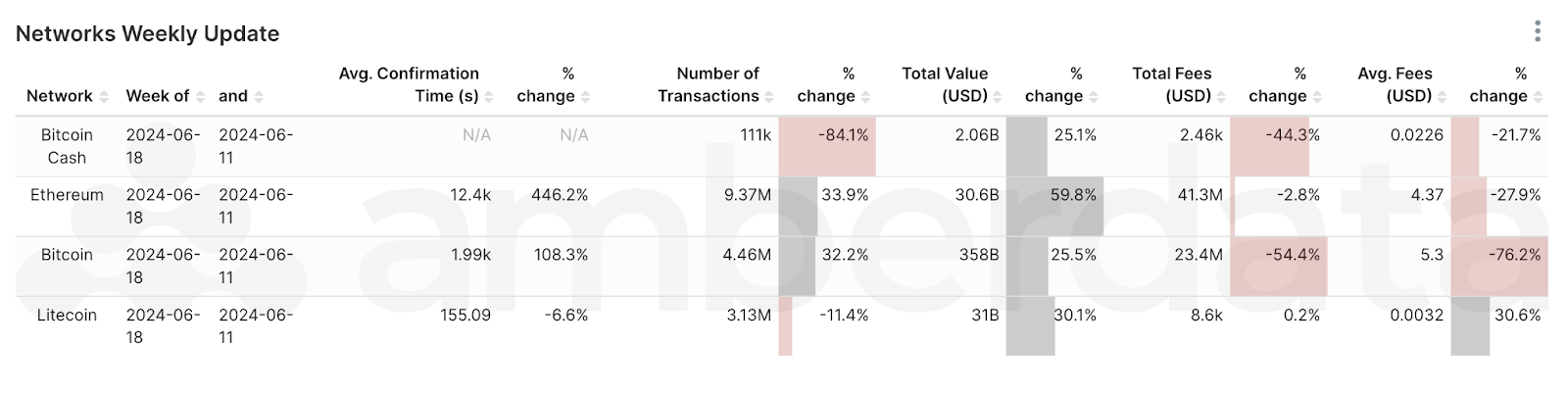

Network comparisons from weeks 6/05/2024 and 6/18/2024

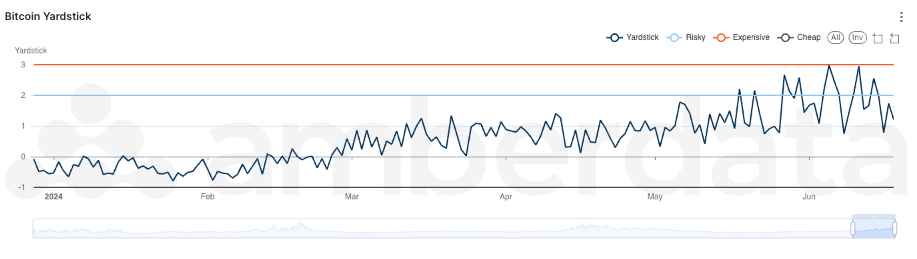

Bitcoin Yardstick from year start to date

The Bitcoin Yardstick is a measure of the value of BTC relative to the amount of energy produced to secure it. Typically, when the yardstick hits values of 2 or 3, it is considered expensive. One interesting thing to note is the behavior of the yardstick throughout 2024’s market cycle. Though it started relatively cheap (i.e. good value for the amount of energy spent to secure it), we have seen with lots of time spent in ATH territory, the price of BTC has almost hit the expensive line several times in the past few months. Typically, this is a good sell indicator, as it may indicate that BTC is overvalued for the amount of energy spent to run the network.

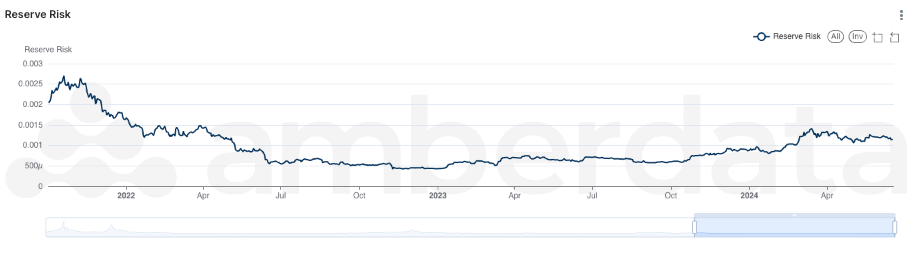

Bitcoin Reserve Risk over the past two years

Context is important when looking at sell indicators. For example, compared to the last bull run, BTC is relatively less risky than the previous ATH market cycle. Of course, relative to the current market cycle, we can see that reserve risk is higher than at the start of the year. When investing in a volatile asset such as Bitcoin, it’s important to contextualize decisions in the frame of current market conditions versus previous conditions to better understand what part of the cycle we are in. Essentially, now is not a bad time to secure a profit, but there is still a good chance that the price of Bitcoin will continue to rise, especially with the Spot ETH ETFs on the horizon.

Links

AmberLens: intelligence.amberdata.com

Recent from Amberdata

- Amberdata: Curve Your Enthusiasm: Curve and the Curve Ecosystem DeFi Primer

- Amberdata: What Institutional DeFi Lenders Need to Know about Overcollateralization

Spot Market

Spot market charts were built using the following endpoints:

- https://docs.amberdata.io/reference/market-metrics-exchanges-volumes-historical

- https://docs.amberdata.io/reference/market-metrics-exchanges-assets-volumes-historical

- https://docs.amberdata.io/reference/get-market-pairs

- https://docs.amberdata.io/reference/get-historical-ohlc

Futures

Futures/Swaps charts were built using the following endpoints:

- https://docs.amberdata.io/reference/futures-exchanges-pairs

- https://docs.amberdata.io/reference/futures-ohlcv-historical

- https://docs.amberdata.io/reference/futures-funding-rates-historical

- https://docs.amberdata.io/reference/futures-long-short-ratio-historical

- https://docs.amberdata.io/reference/swaps-exchanges-reference

- https://docs.amberdata.io/reference/swaps-ohlcv-historical

- https://docs.amberdata.io/reference/swaps-funding-rates-historical

DeFi DEXs

DeFi DEX charts were built using the following endpoints:

- https://docs.amberdata.io/reference/defi-dex-liquidity

- https://docs.amberdata.io/reference/defi-dex-metrics

- https://docs.amberdata.io/reference/defi-impermanent-loss

DeFi Borrow/Lend

DeFi lending charts were built using the following endpoints:

- https://docs.amberdata.io/reference/defi-lending-protocol-lens

- https://docs.amberdata.io/reference/defi-lending-asset-lens

Networks

Network charts were built using the following endpoints:

- https://docs.amberdata.io/reference/blockchains-metrics-latest

- https://docs.amberdata.io/reference/transactions-metrics-historical

- https://docs.amberdata.io/reference/get-historical-transaction-volume