Share this blog:

Markets are on edge ahead of fresh CPI and PPI data, with the Fed still split on the timing of potential rate cuts. Tariff escalations and rising Treasury yields are adding pressure, while Bitcoin pushes to new all-time highs alongside renewed institutional flows.

Read more for the full macro and crypto breakdown →

USA Week Ahead (ET):

-

Tuesday 8:30am - CPI

-

Tuesday - *Various Fed Governors Speak

-

Wednesday 8:30am - PPI

-

Wednesday 2pm - Fed Beige Book

-

Wednesday - *Various Fed Governors Speak

-

Thursday - *Various Fed Governors Speak

Visit Amberdata.io

Disclaimer: Nothing here is trading advice or solicitation. This is for educational purposes only.

Authors have holdings in BTC, ETH, and Derive and may change their holdings anytime.

![]()

MACRO Market Overview

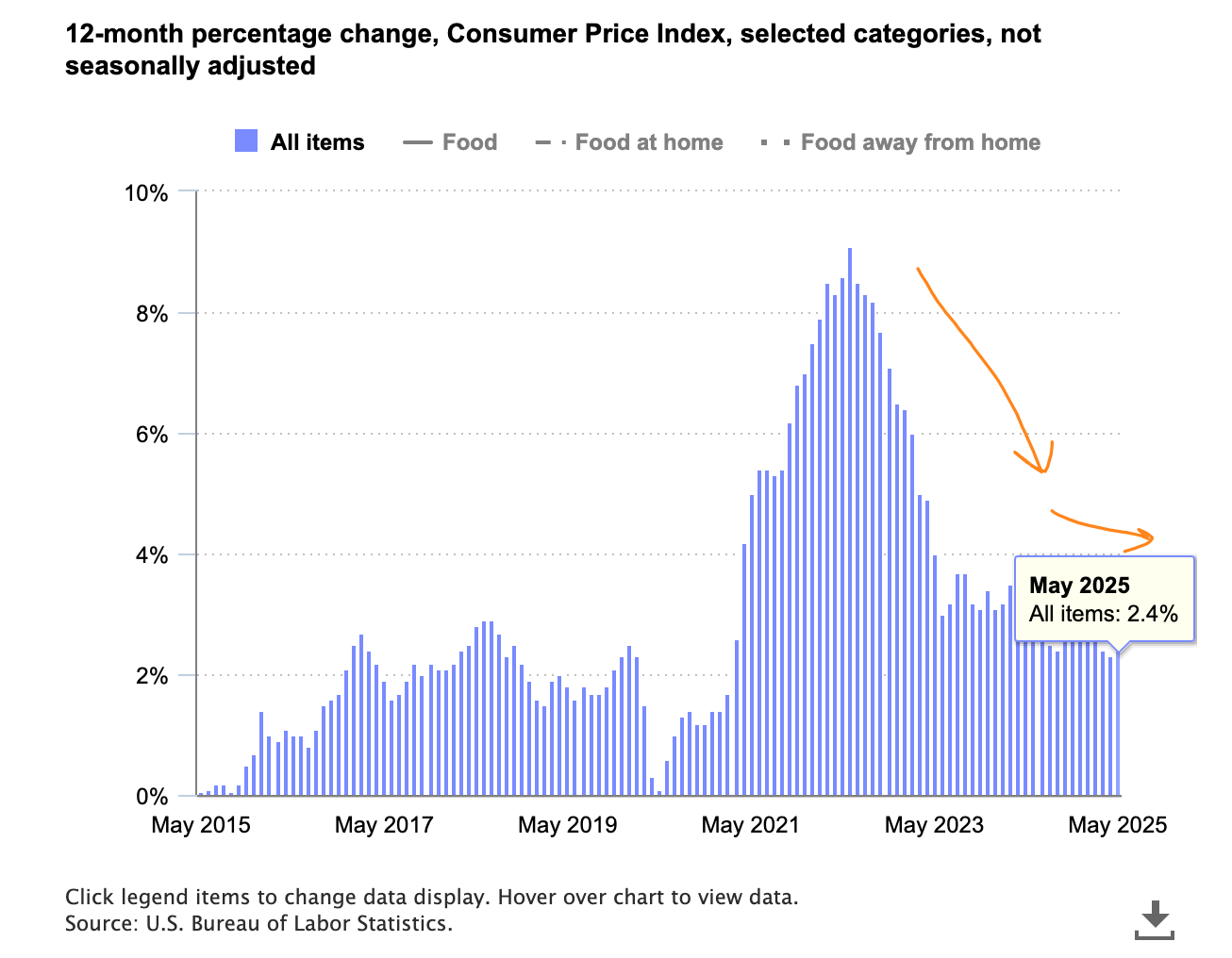

This upcoming week we have inflation data set to hit the wires. On Tuesday we will have CPI followed by PPI on Wednesday.

The most recent CPI reading (for May 2025) came in at +2.4% annualized, as inflation continues to trend lower post pandemic.

Chart: Consumer Price Index via bls.gov

On Wednesday of last week, the FOMC minutes for the May rate decision were released. This recap highlights themes still currently running at the Fed.

Essentially the Fed thinks it’s well positioned to continue the "wait and see" approach, despite the large drop in CPI since 2021 and 2022.

The minutes revealed a wide range of thoughts on the likely path of interest rates for the rest of the year, as it’s still very unclear to the Fed how tariffs will impact inflation.

Most Fed officials see some rate cut as appropriate this year with Fed Governors Michelle Bowman and Chris Waller being the most “Dovish” governors. They have publicly said they might be open to a rate cut as early as the July meeting.

The dovish argument relies upon a materializing weakness in labor markets combined longterm inflation expectations continuing to be well anchored.

Chart: 10y inflation expectations

What scares the Fed most is the possibility that inflation could be more persistent while at the same time that employment weakens, which would present "difficult tradeoffs" for the FOMC (More on this “Stagflation” in the BTC analysis next)

Tariffs escalations

The April Liberation Day tariffs imposed a universal 10 % tariff, with reciprocal rates up to 50 % for 57 nations. As the market dropped the Admin cooled away from hardline tariffs to settle at 10%.

Now 30% “headline” tariffs are being discussed on EU, Mexico, and Canada.

As long as markets continue to remain strong, Trump is likely ready to push harder along these lines.

One area we would watch closely is how the bond market reacts to increased pressure. Reducing trade deficits (through tariffs) means there is less cash for foreign investors to recycle into Treasuries, which is especially crucial for Japan (Historically the largest buyer of US Treasuries).

Higher treasury yields continue to narrow the equity risk premium and raise government budget financing costs.

This will also put pressure on Powell to reduce rates. Trump wants to fund the US debt with T-Bills (the Fed can control short-term rates) in order to reduce US debt financing costs.

Japan & US trade negotiations went sideways last week as Trump announced 25% tariffs on all imports. Japan is refusing to bend.

This is crucially important in my opinion as Japan’s outstanding debt/gdp has always been a big red flag!

Yields can’t afford to go up, but a large trade surplus has allowed them to remain strong, accumulating FX reserves and buying US Treasuries with those reserves… How does a trade war with Japan affect this dynamic? Could this trigger debt problems?

Chart: ZeroHedge.com / Bloomberg Chart

BTC: $119,008 (+9.2% / 7-day)

ETH :$2,998 (+17.7% / 7-day)

SOL :$163.12 (+7.0% / 7-day)

Crypto Options Overview

After the initial tariff shocks and the Liberation Day crash, traders have now seen a full recovery in risk assets. NVDIA officially became the first company to cross a $4T market cap.

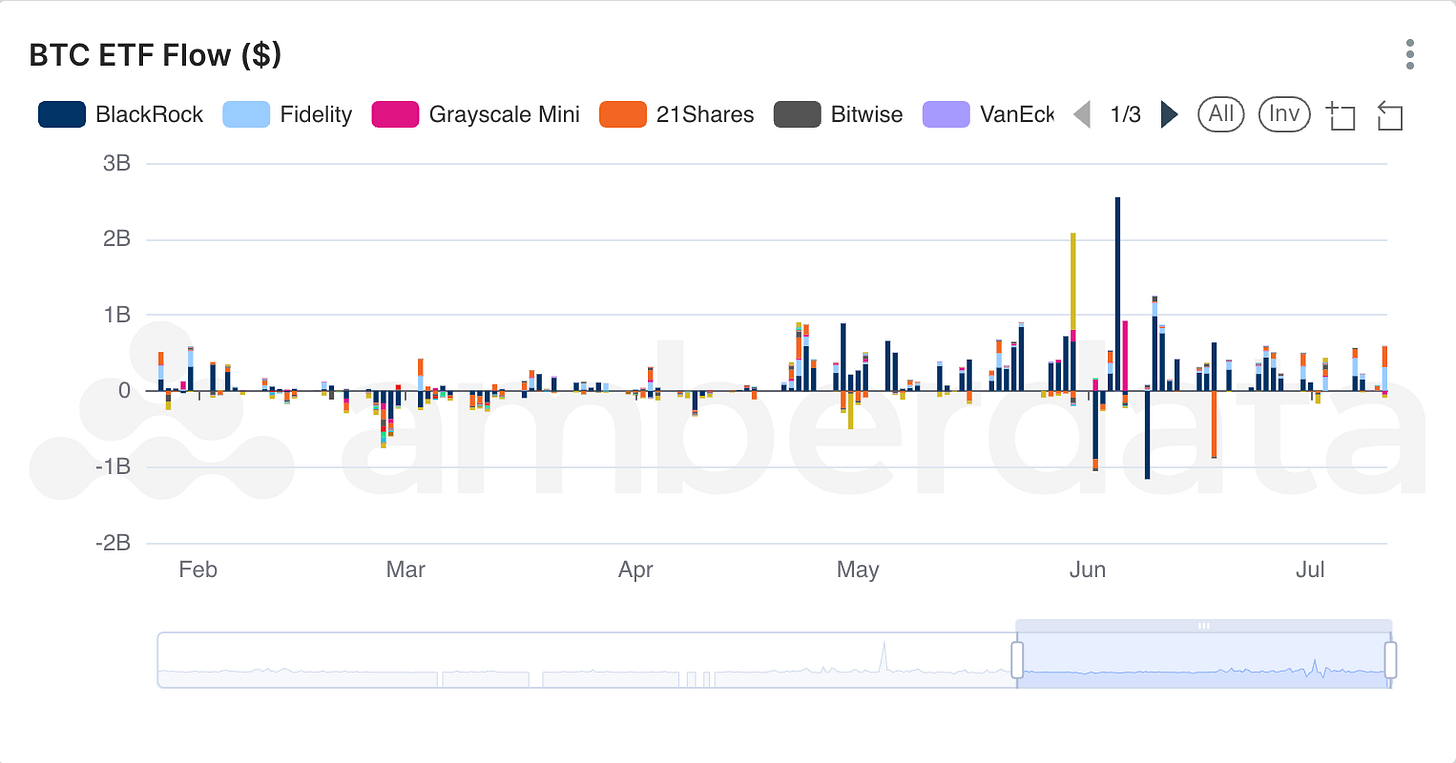

BTC has been rallying alongside the recovery in tech stocks and equities with participation of institutional traders in the IBIT ETF, as ETF flows continue to come in.

Chart: BTC ETF Flows (intelligence.amberdata.com)

These themes describe the current movement into new ATHs, in a manner much more controlled than past bull-market highs (think Q4 2020).

From a fundamental perspective however, BTC is also a form of "digital gold", where-as most other crypto assets trade as pure "risk-on" securities.

The recent FOMC minutes showed Fed governors remain concerned about the potential for stagflation. This would be persistent inflation due to global trade and in tandem with weakness in employment (which has yet to materialize).

The last known stagflation episode was in the 1970s when Nixon ended the gold standard and inflation come in hot.

This sent gold from $35/oz in 1970 to $671/0oz by 1980... Almost 20x in 10yrs.

Chart: GOLD 1970 → 1980 (TradingView.com)

The market seems to be hedging the same risks the Fed fears... As US budgets continue to balloon and inflation remains top-of-mind (think BBB) Gold has rallied to $3370 while both Platinum and Silver are at multi-year highs... This means BTC's digital gold narrative remains extremely attractive.

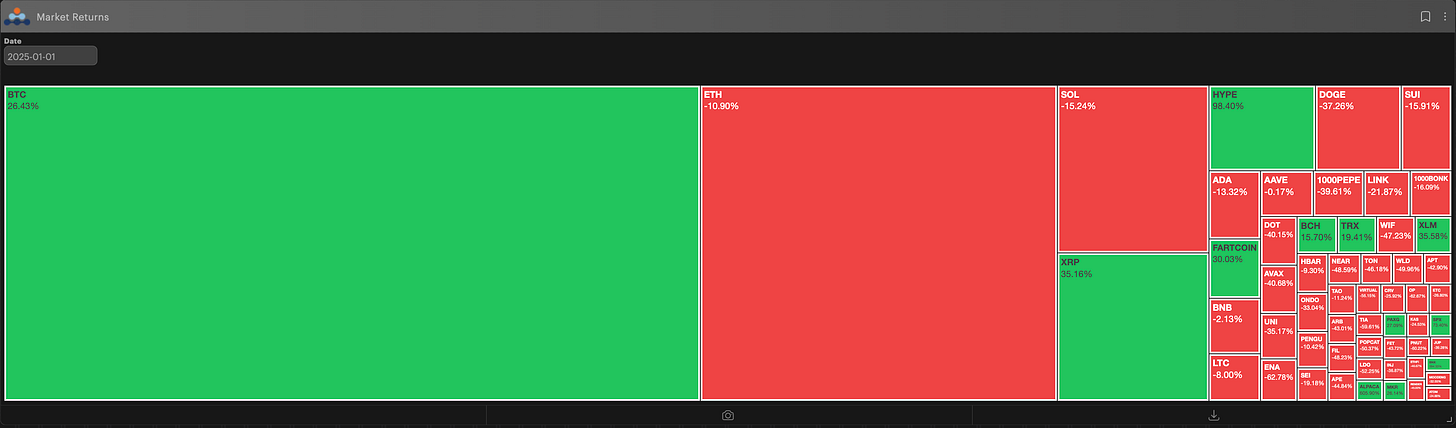

Currency YTD Returns (pro.amberdata.io)

Compared to other crypto assets (see chart above) we can see BTC is specifically an outperforming asset in the crypto sector, further confirming the digital gold narrative.

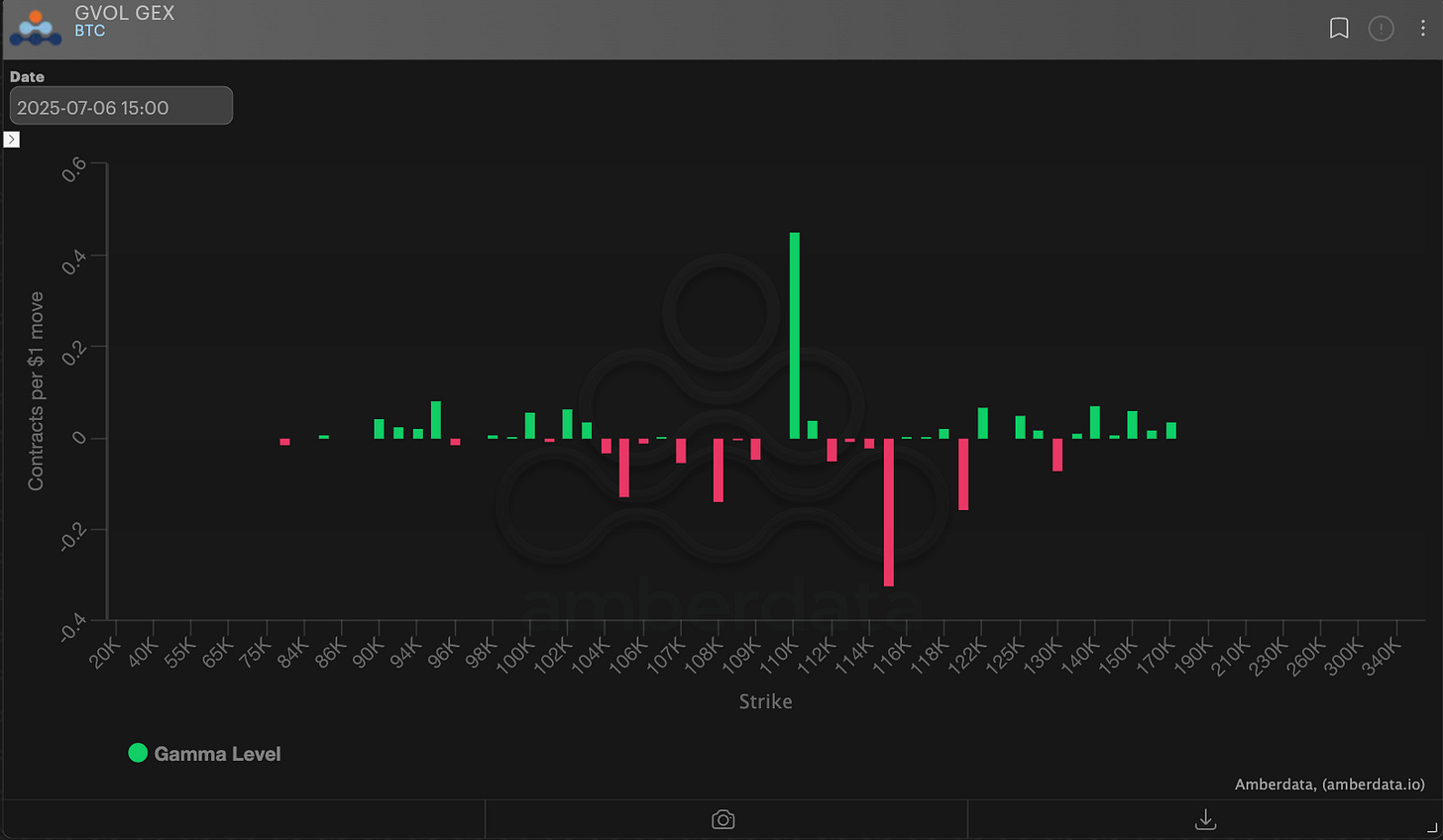

Last Sunday, the street was short a lot of volatility right at the previous ATH of $110k. Lower volatility into the summer months was a logical bet, especially given the recent doldrum in volatility.

Chart: GEX Last week 7/6/2025 (pro.amberdata.io)

As BTC broke new ATHs and upside volatility finally came back to the market, we’ve seen one of the largest “buy-to-close” liquidation events in a long time.

Chart: Futures and Perp liquidations (pro.amberdata.io)

Short delta traders were forced out of their positions helping markets move higher and reprice funding (and futures basis) higher as well.

Chart: BTC 30-dte basis (pro.amberdata.io)

Futures basis nearly double for 30 days-to-expiration, from 3.50% annualized → 7.50% across major venues. This alone is an interesting trade when risk-free treasuries sit at 4.30%.

Chart: Deribit DVOL index (pro.amberdata.io)

Despite the strong ATH breakout, BTC implied volatility hasn’t moved much higher, at least in the broader context.

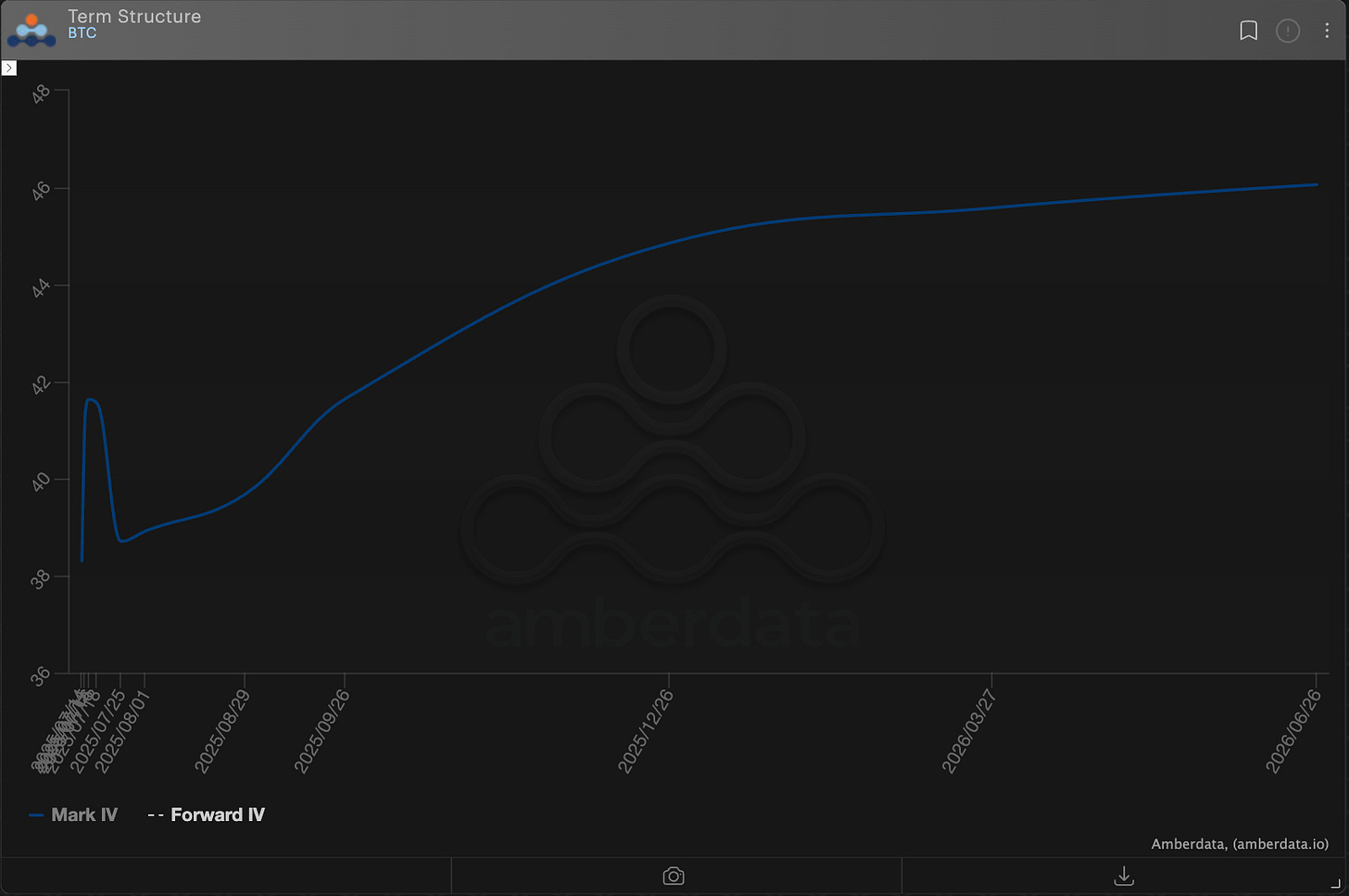

Chart: BTC term structure (pro.amberdata.io)

The BTC at-the-money volatility term structure is still in Contango. Historically speaking the steepness of the current Contango is also showing gamma is “cheap” here, should there be any continued move higher (or puke reversal).

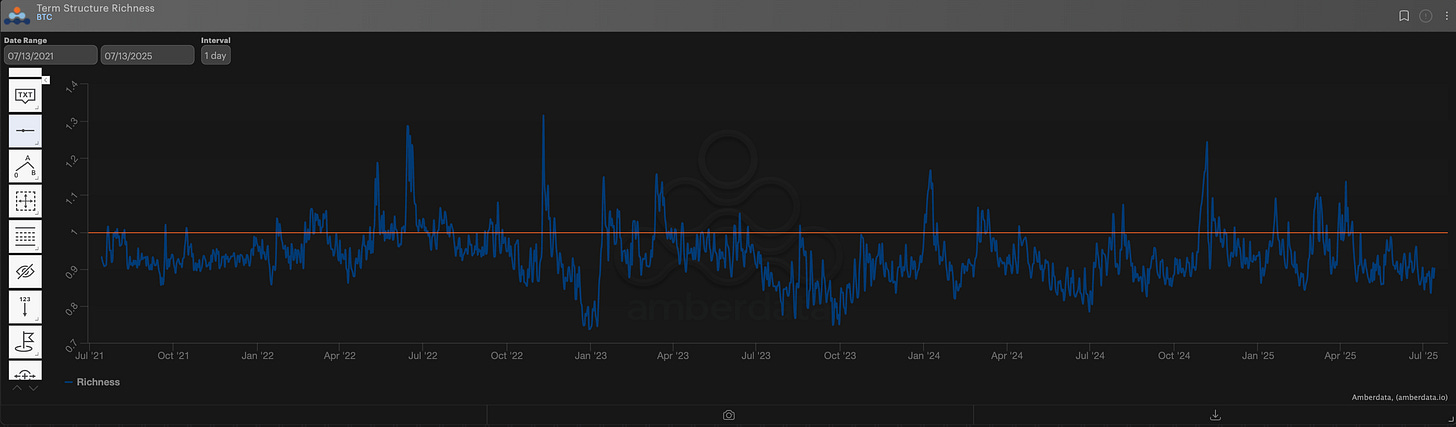

Chart: BTC Term Structure Richness (pro.amberdata.io)

We can see the term structure richness chart (above) shows a lot of room to run higher, if the term structure was going to touch backwardation of any sort (1.00 reading = Flat Term structure).

ETH could continue to explode higher too, as I imagine a lot of traders cut ETH exposure after the past 24-months of pain, creating side-lined buy pressure.

Overall, short-term option gamma seems like the highest asymmetric trade at the moment. Spot is moving, basis is moving and vol has yet to really move.

That said, I personally find these trades hard to manage… You’re racing against the clock and it’s hard to gauge WHEN to take off a profitable trade.

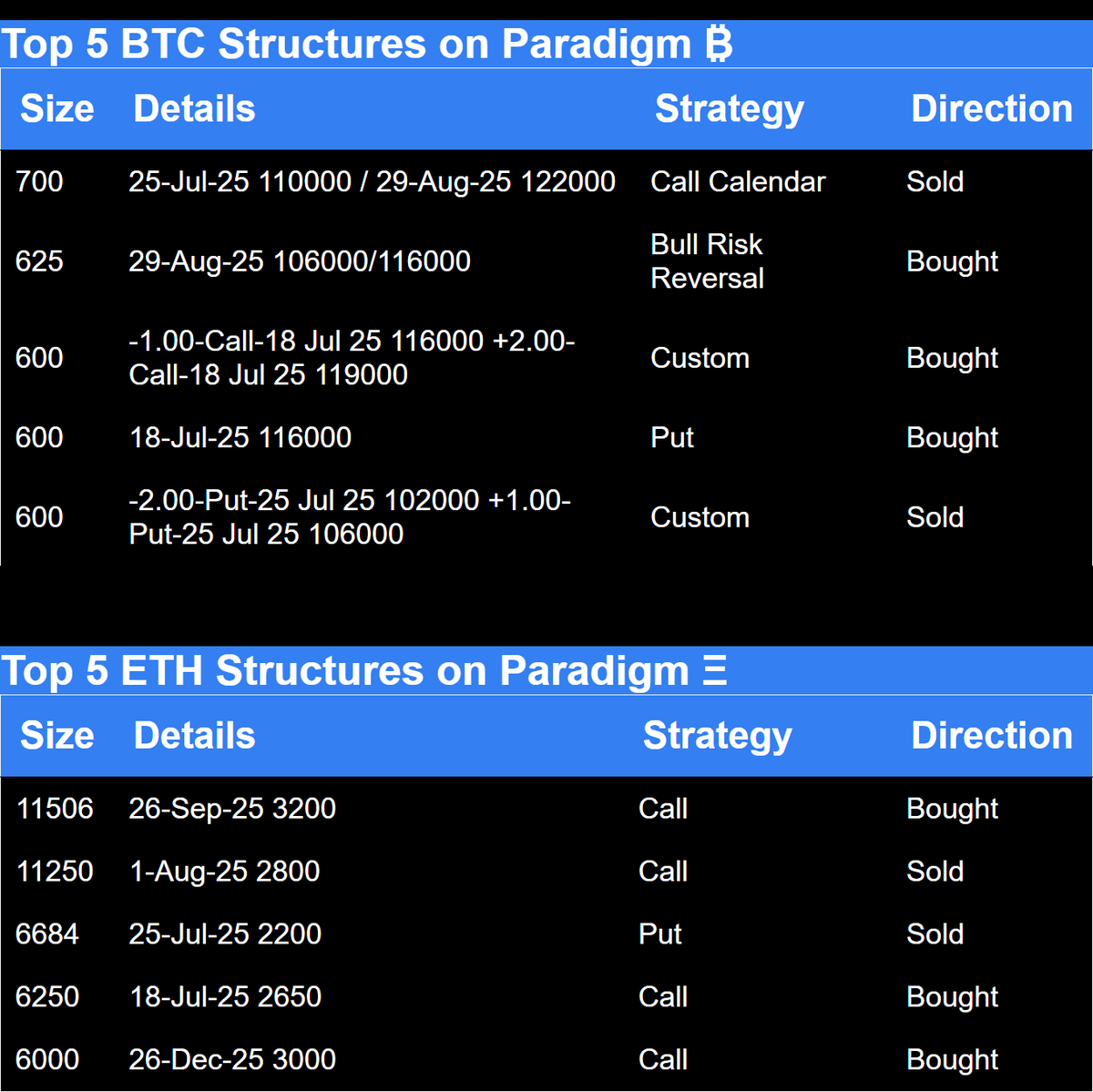

Paradigm Weekly Overview

Paradigm Top Trades

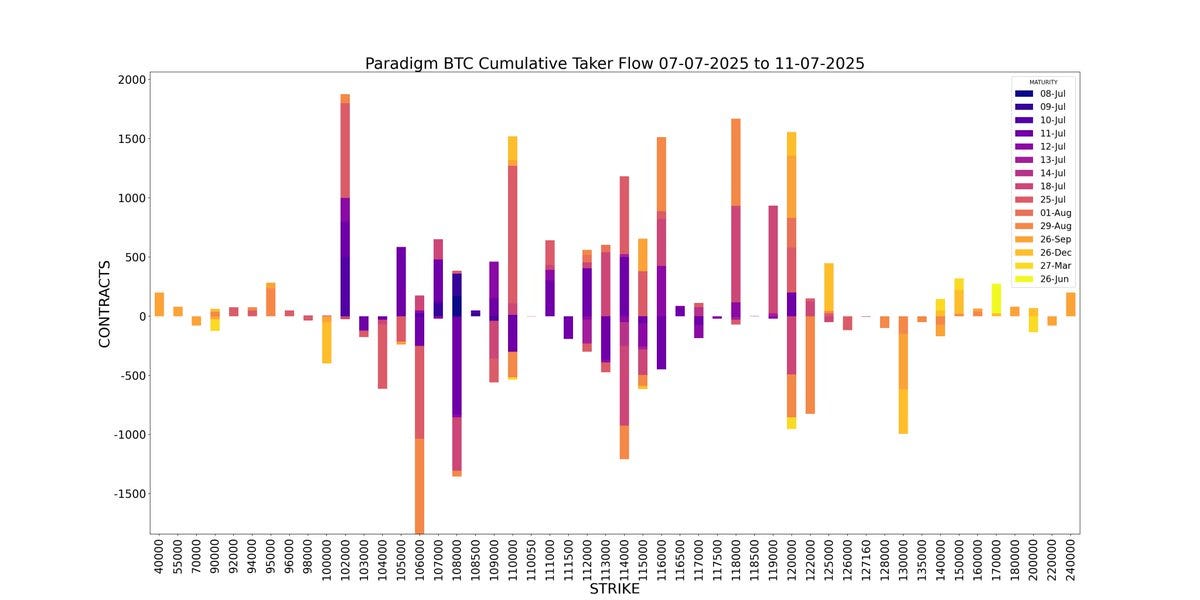

BTC Cumulative Taker Flow

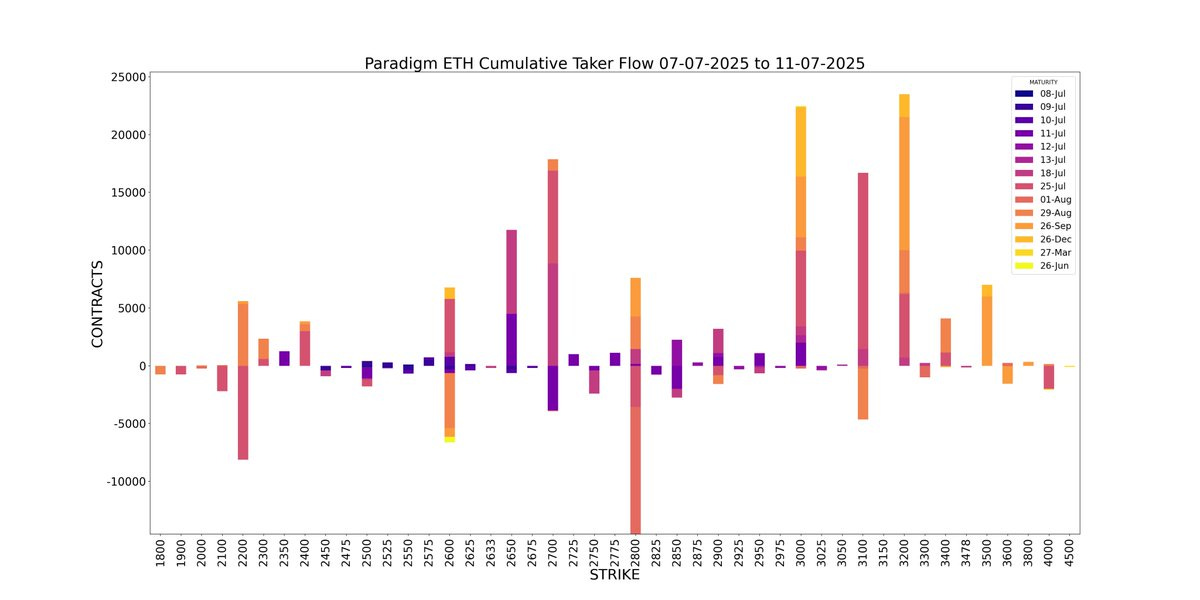

ETH Cumulative Taker Flow

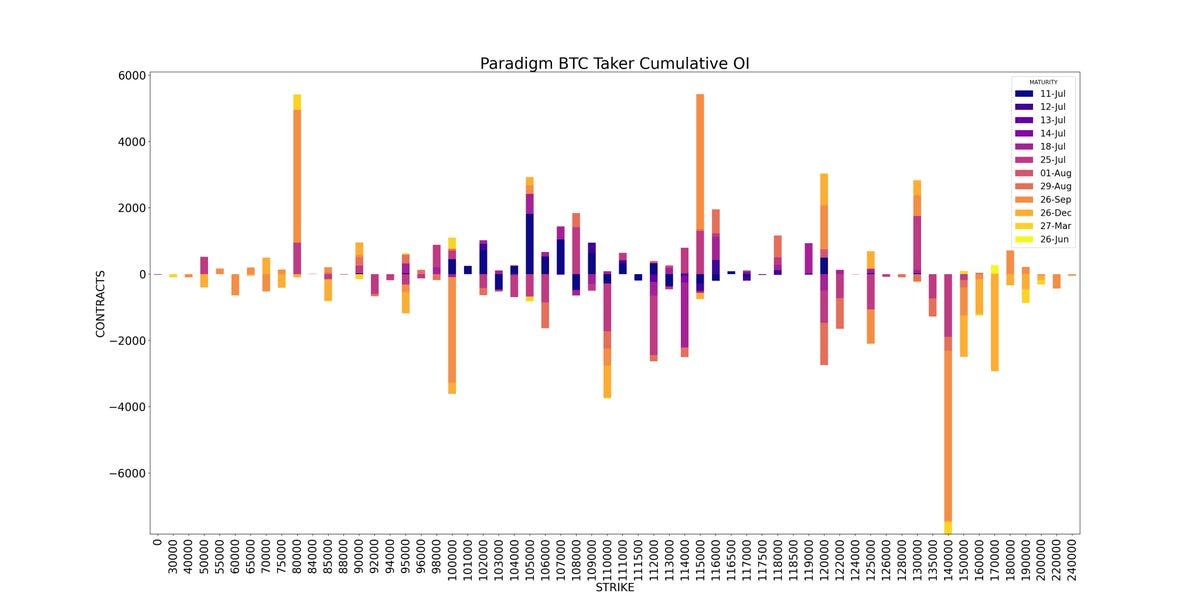

BTC Cumulative OI

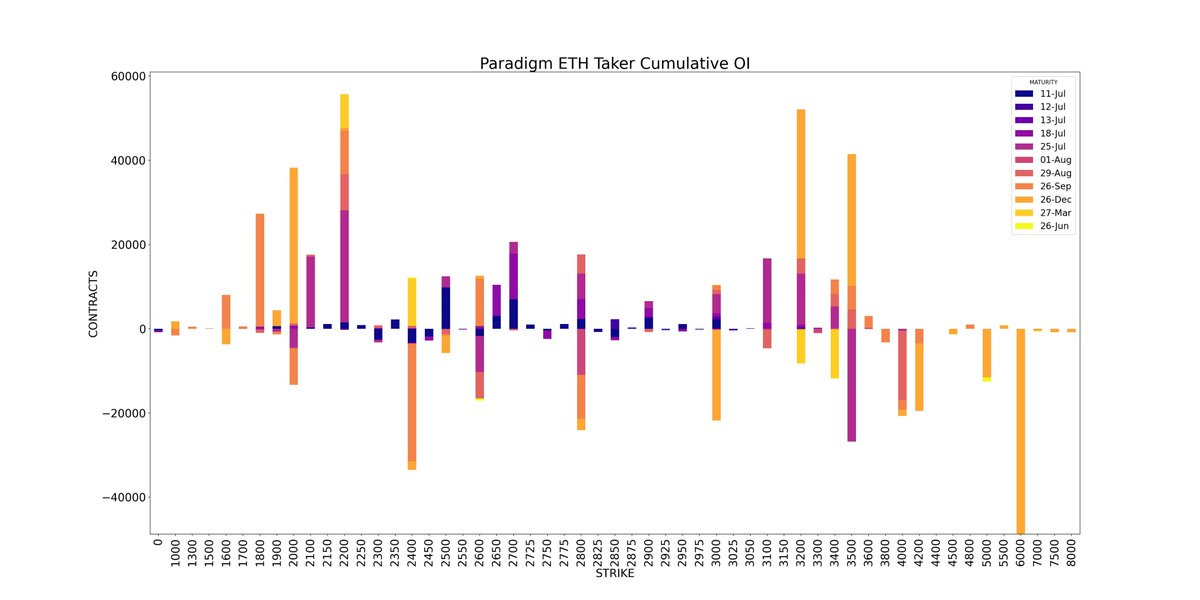

ETH Cumulative OI

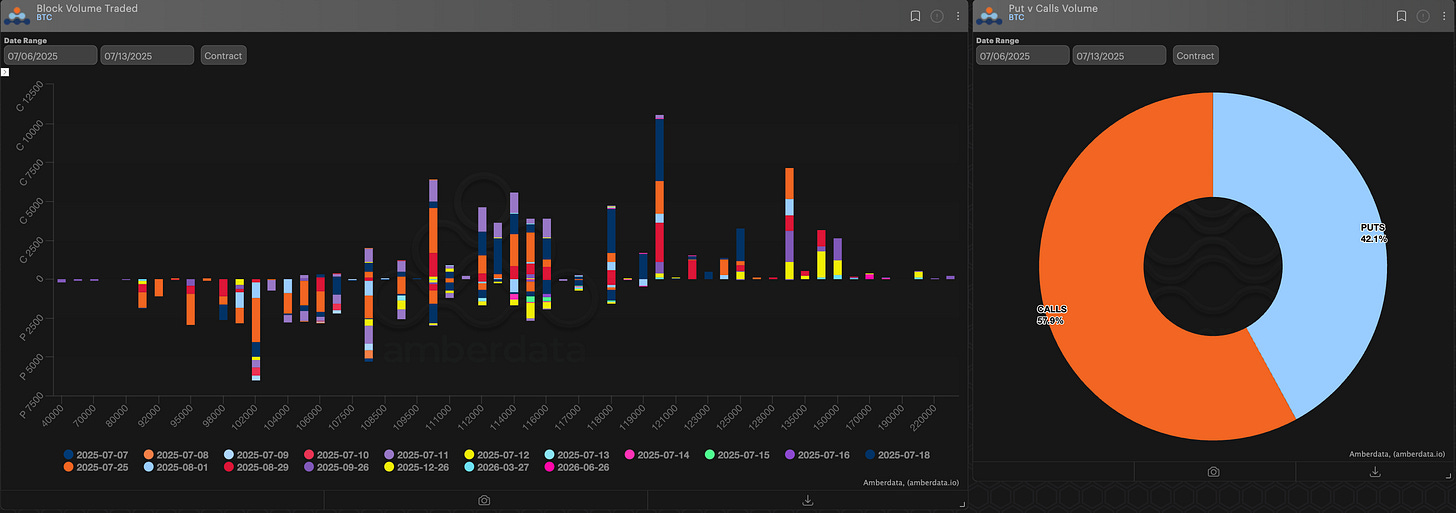

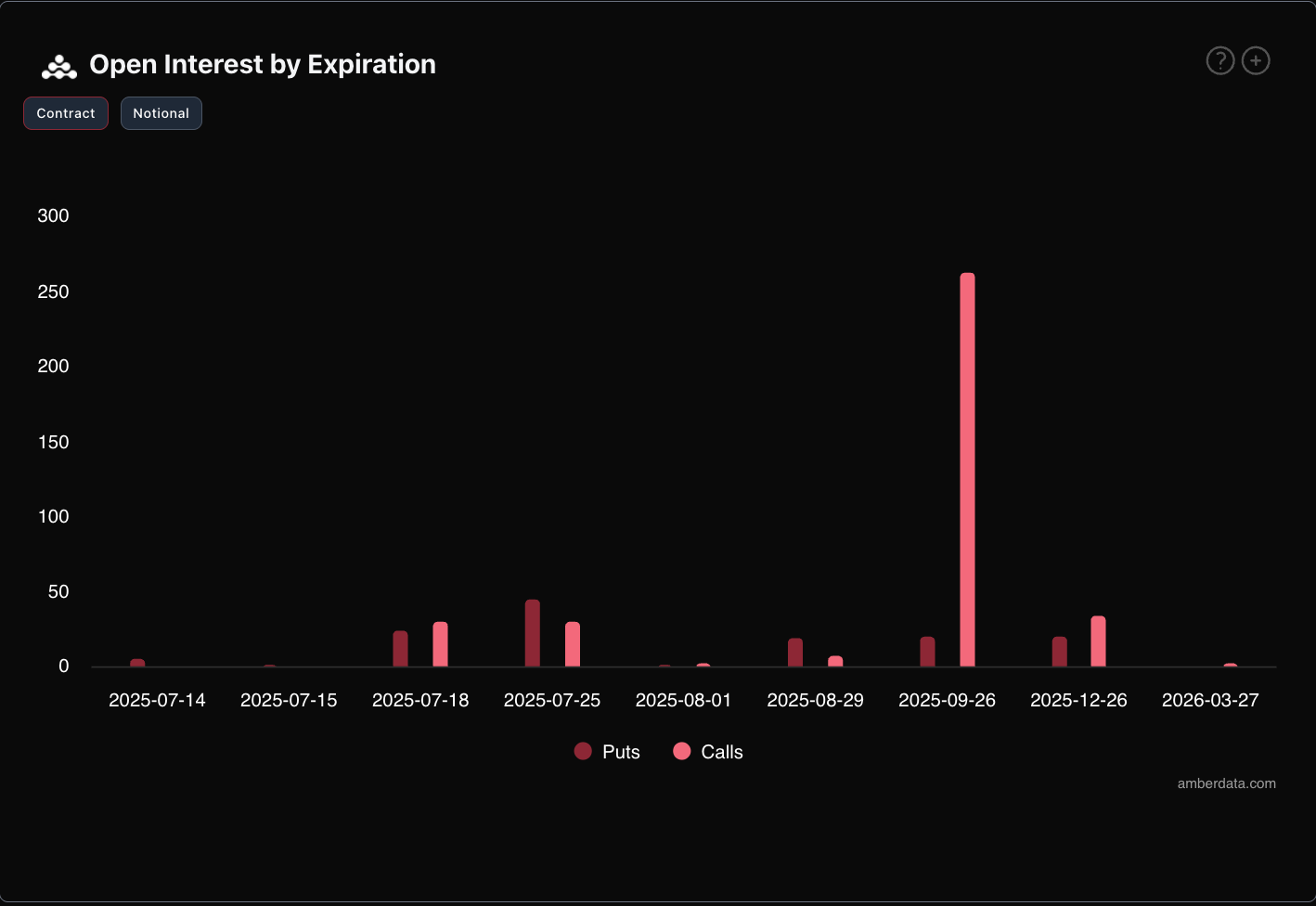

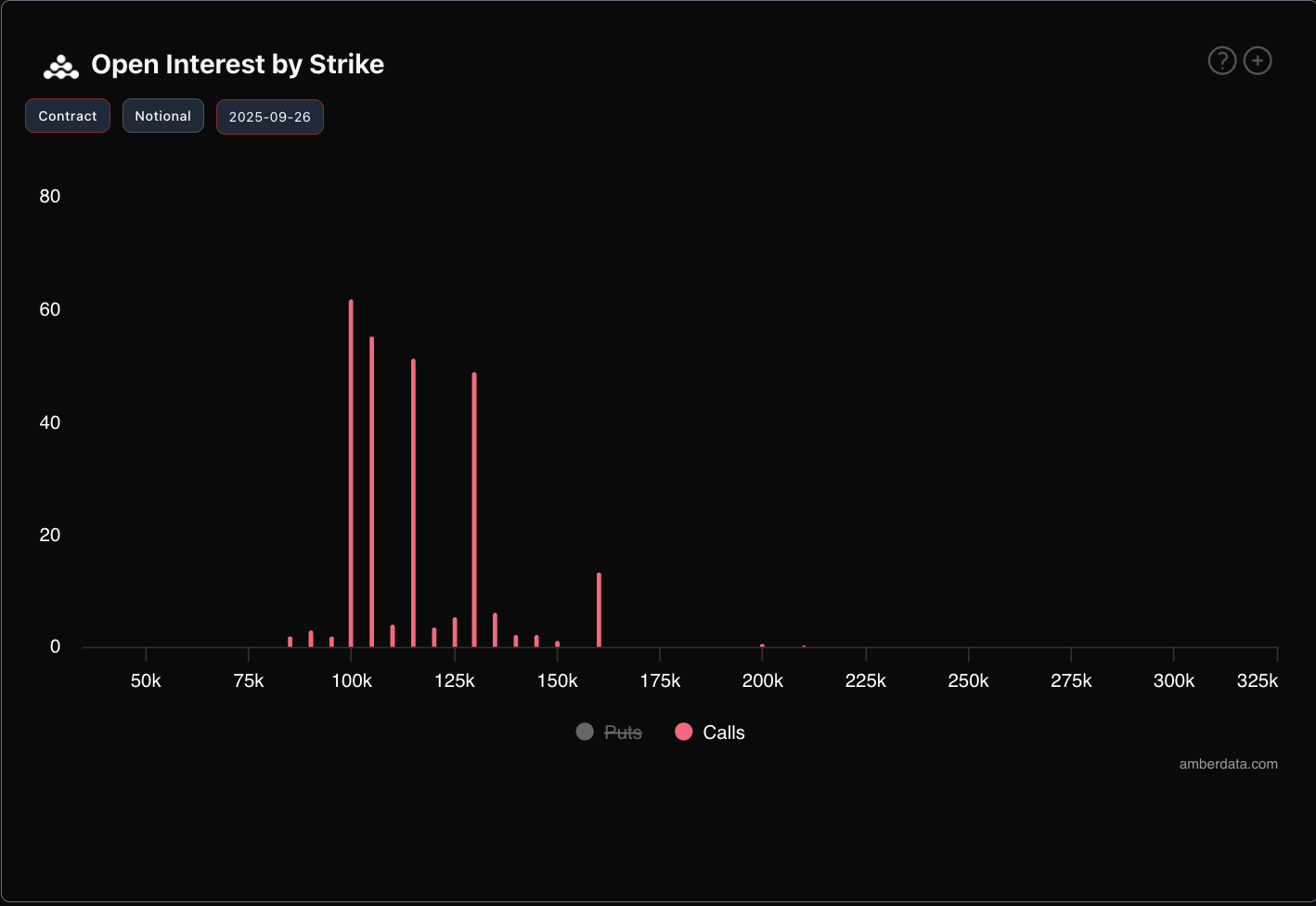

BTC

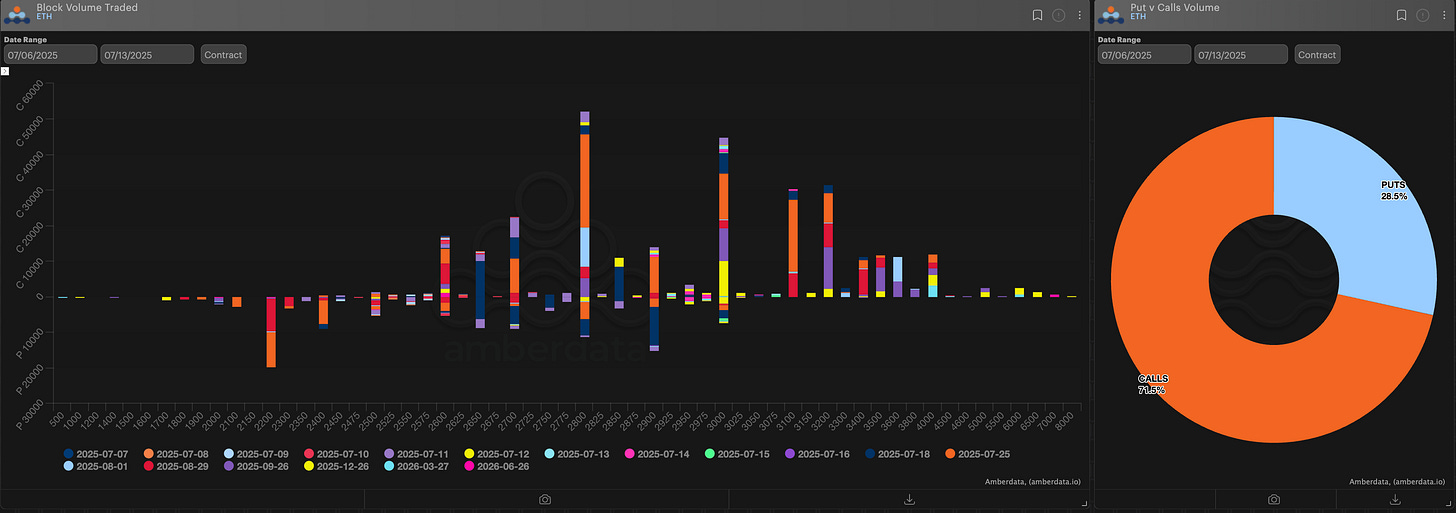

ETH

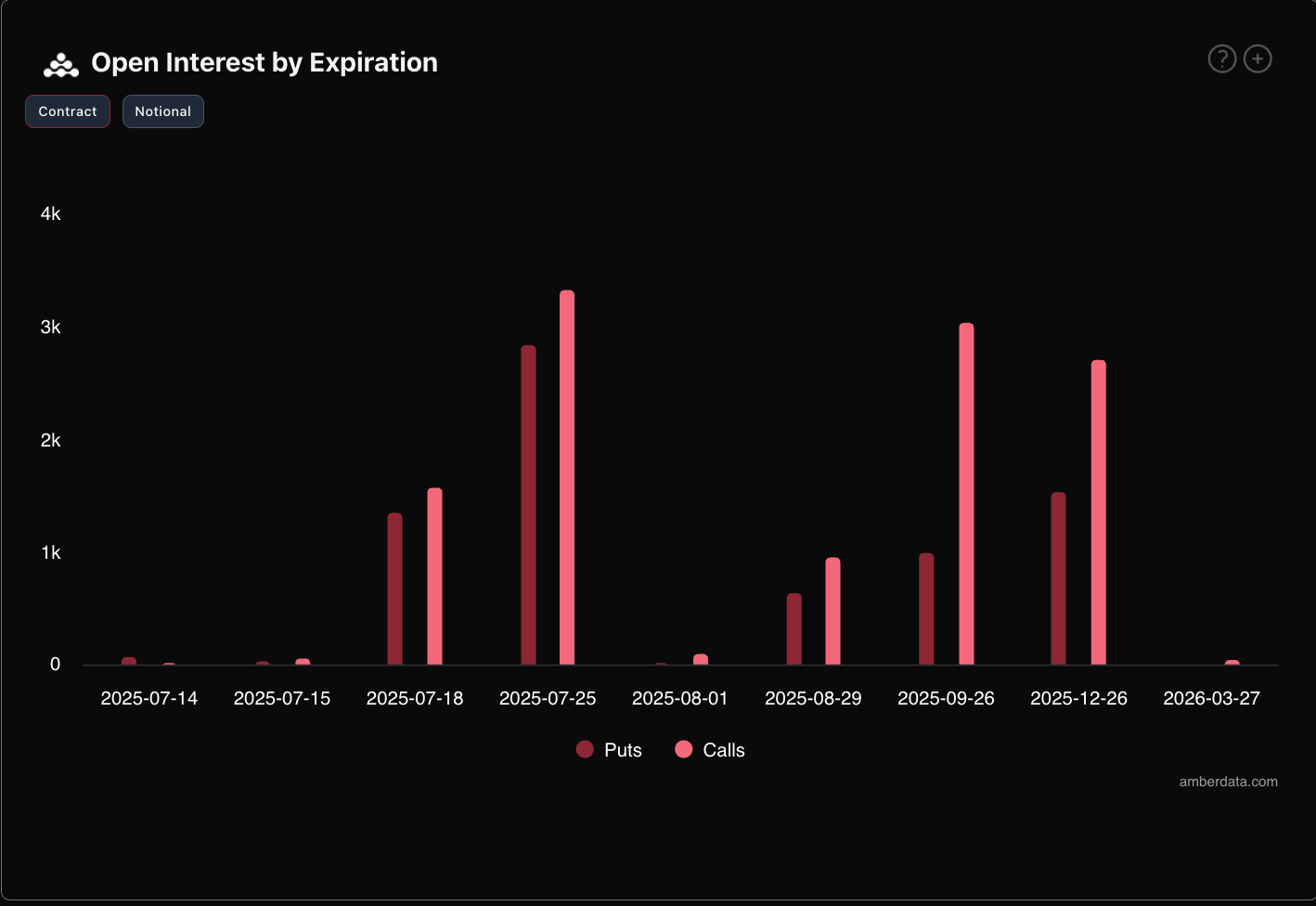

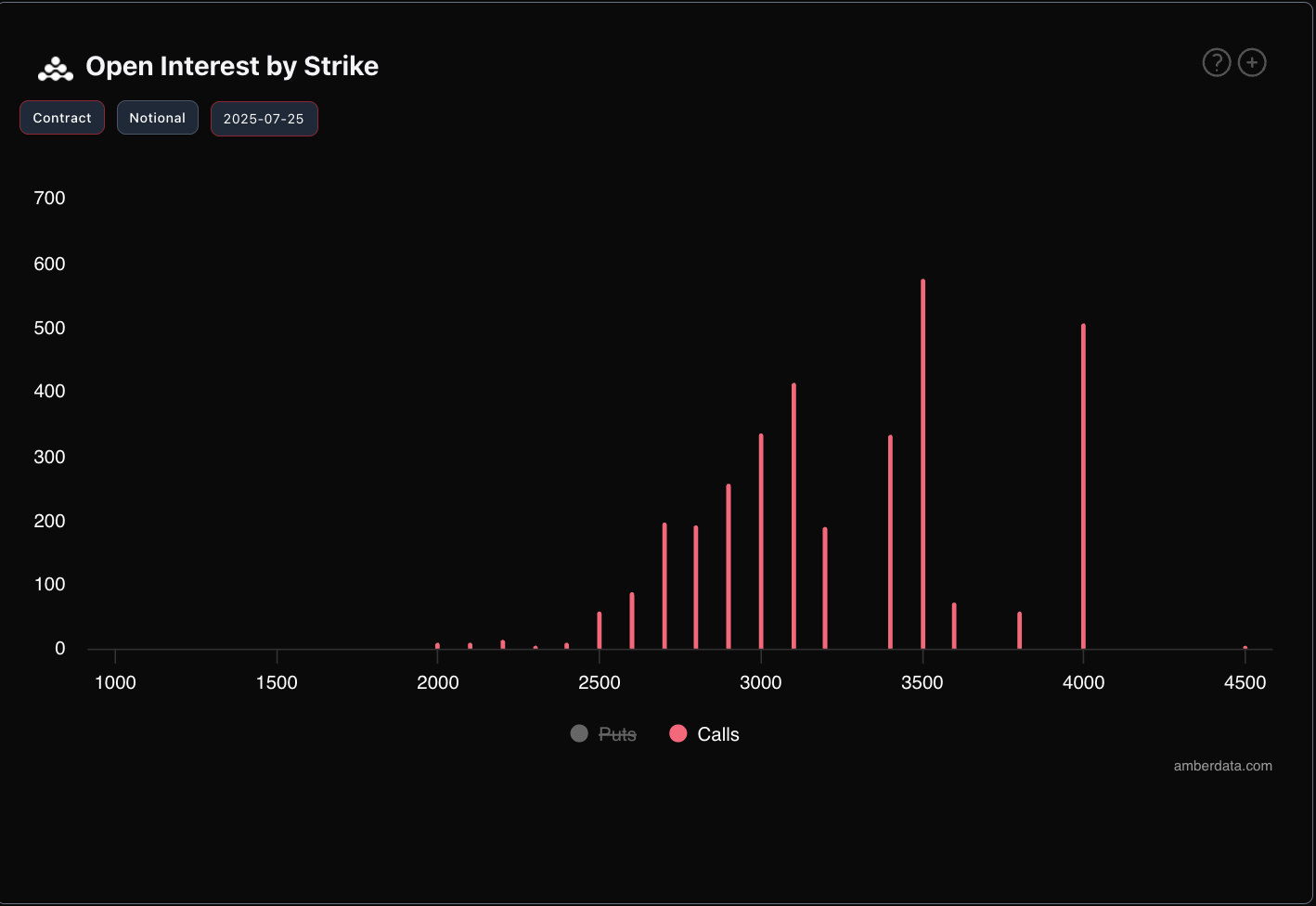

DeFI options traders in Derive.xyz are concentrated in “medium term” September expirations.

Call strikes around $130k seem to be next price level in play here.

ETH defi traders however are trading more for gamma and continued upside. Call options are concentrated in the 7/25 expiration cycle.

Strikes of interest go from $3,000 → $3,500 → $4,000 which means at least some expect good follow—through to the recent rally.

AMBERDATA DISCLAIMER: The information provided in this research is for educational purposes only and is not investment or financial advice. Please do your own research before making any investment decisions. None of the information in this report constitutes, or should be relied on as a suggestion, offer, or other solicitation to engage in, or refrain from engaging, in any purchase, sale, or any other investment-related activity. Cryptocurrency investments are volatile and high risk in nature. Don't invest more than what you can afford to lose.