Share this blog:

In this week's analysis, get insights on the latest crypto market trends, macroeconomic factors, and key upcoming events impacting Bitcoin, Ethereum, and other digital assets. Last week, stocks started strong but ended bearish as bond yields rose, challenging expectations of lower volatility. Meanwhile, a hot employment report shifted rate cut probabilities for the upcoming FOMC decision.

USA Week Ahead (ET):

-

Tuesday 8:30a - PPI

-

Tuesday 2p - Fed Beige Book

-

Wednesday 8:30a - CPI

-

*Various Fed Governors speak during the week*

Visit Amberdata.io

Disclaimer: Nothing here is trading advice or solicitation. This is for educational purposes only.

Authors have holdings in BTC, ETH, and Lyra and may change their holdings anytime.

![]()

MACRO Overview

Last week stocks opened strongly and closed very bearishly as bond yields increased. So much for lower volatility!

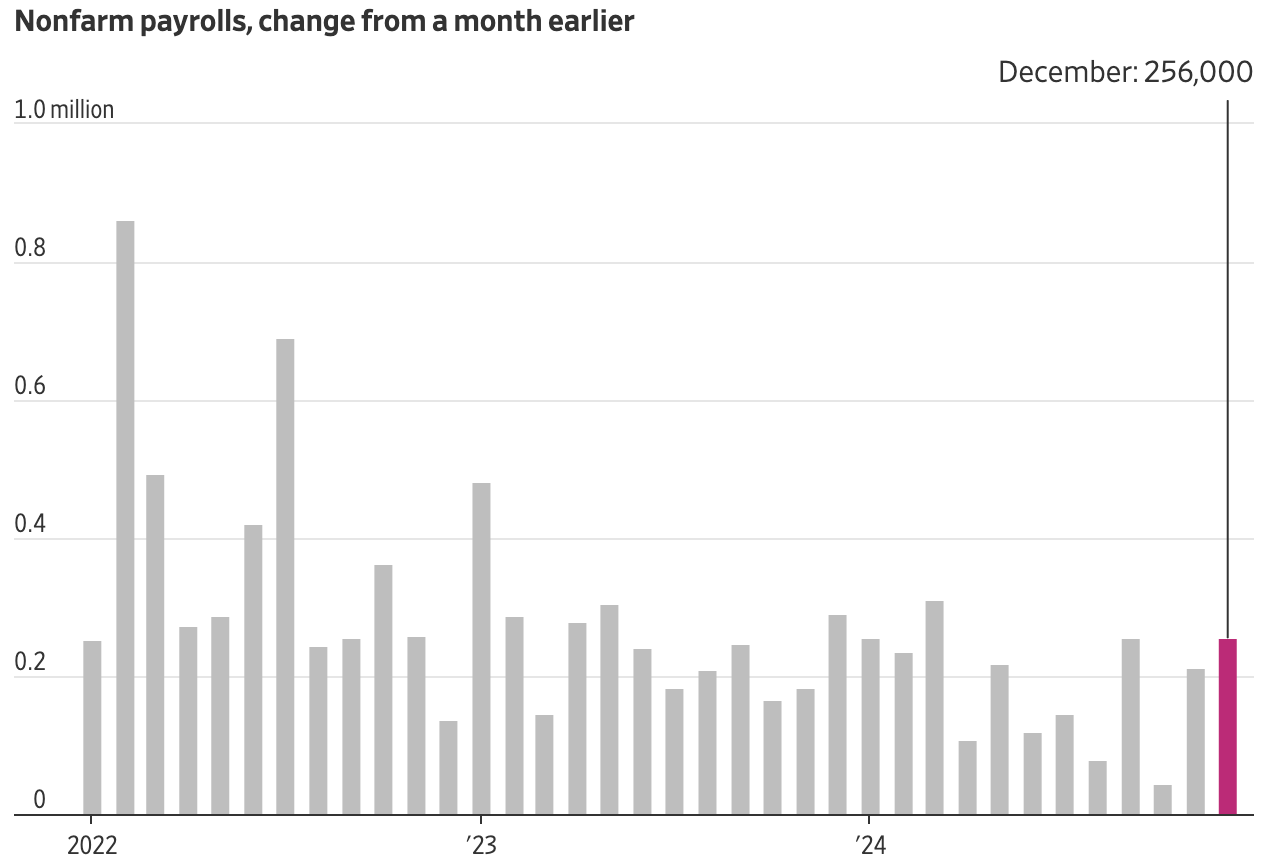

Chart: WSJ.com

The employment situation report came in much hotter than expected on Friday. Economist predicted +155k jobs as the median forecast with a 4.2% unemployment rate from the household survey, instead we got +256k jobs created and a drop to 4.1% unemployment.

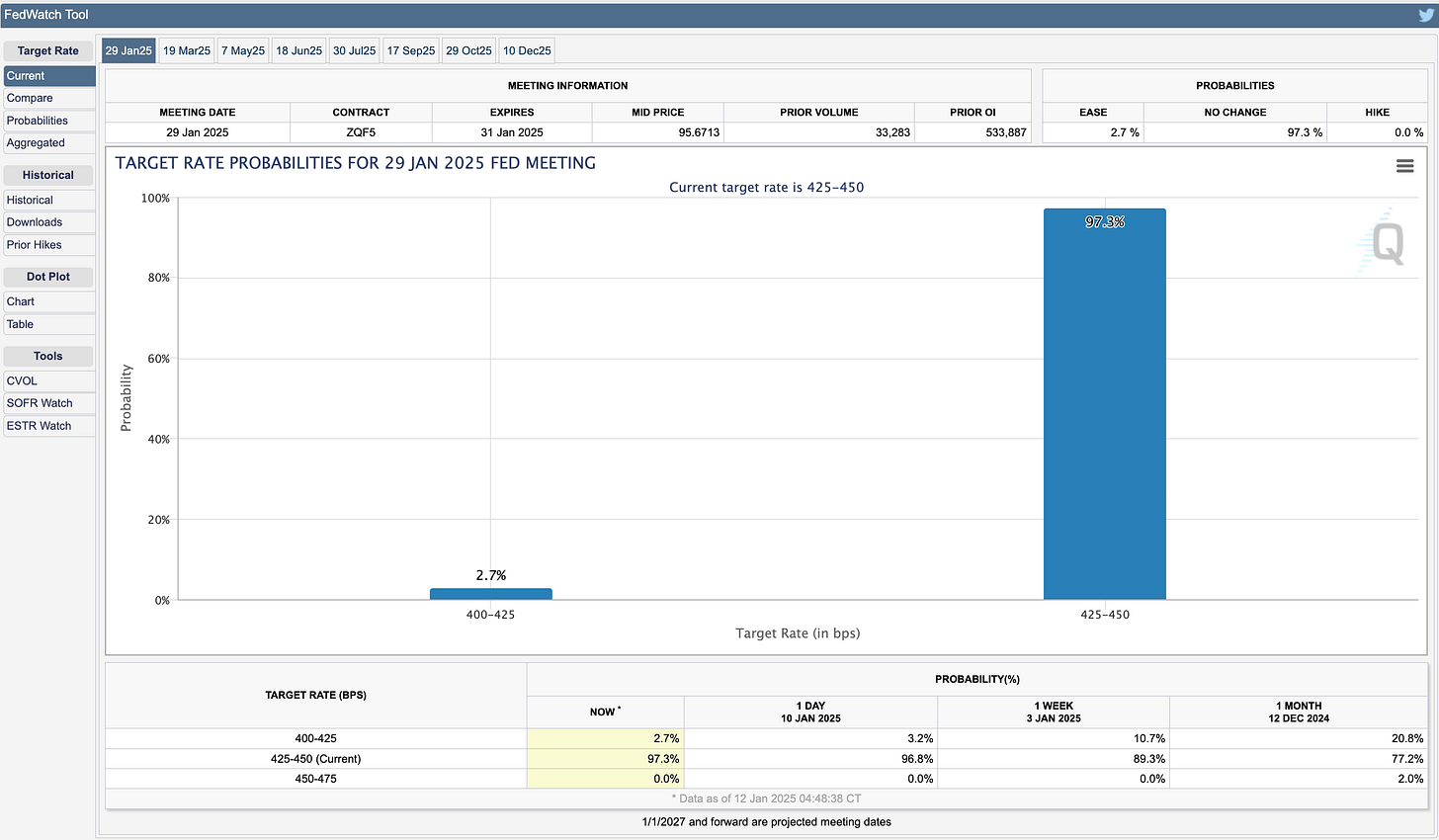

Chart: CME FedWatchTool

As a result, the Jan 29th FOMC rate decision now has a market implied probably of 97.3% to be “unchanged” and only a 2.7% chance of a -25bps cut.

7-days ago there was a 10.7% chance of a -25bps cut, 30-days ago that probability was 21%.

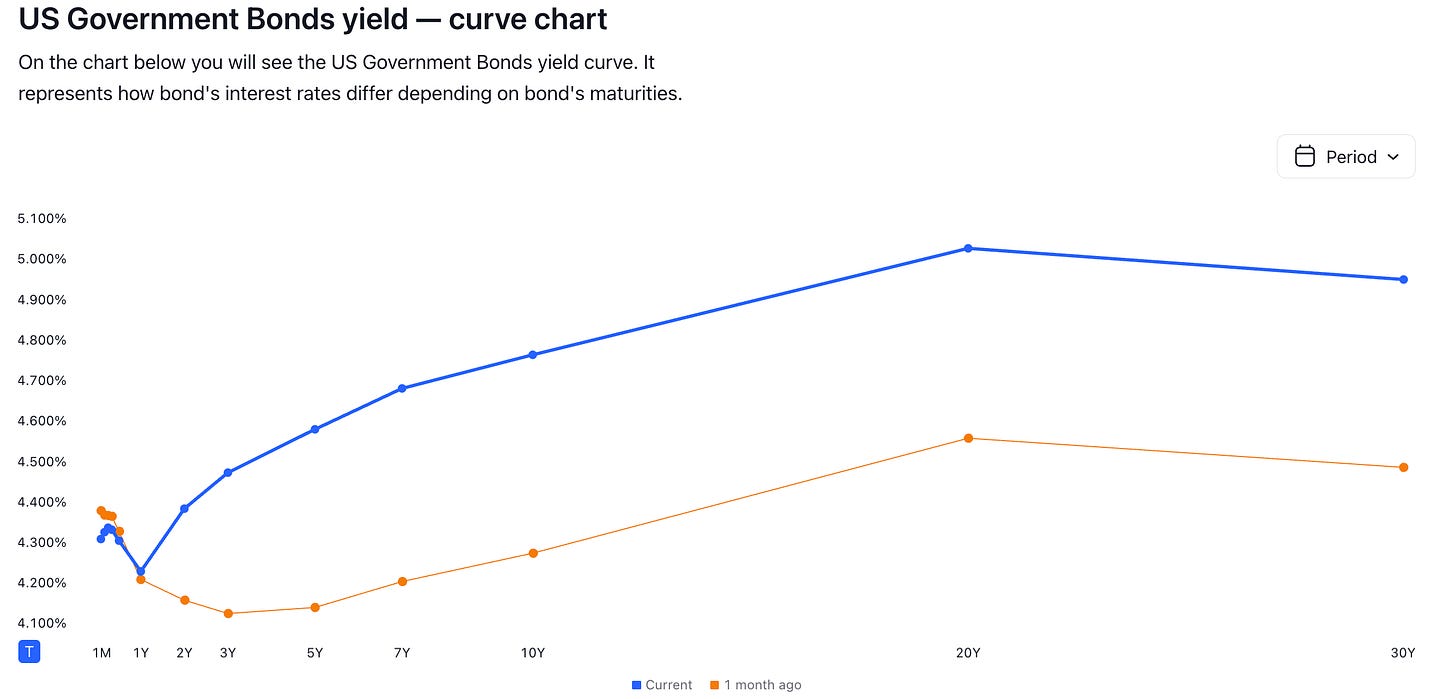

Chart: US Treasury Yield Curve (TradingView.com)

The stock market (and risk-assets) continue to be sensitive to the treasury yield curve and the expectation for future Fed cuts, since the hawkish rhetoric in December’s FOMC.

Last week we also had the FOMC minutes released from the December FOMC. Minutes showed that Fed governors are comfortable holding rates higher for longer.

With a strong labor market, potential price tag inflation from tariffs, and the shrinking of the low-wage labor force from immigration policy reforms… the US rate curve could definitely remain a drag on stocks and risk assets if inflation picks up again.

The VIX index has completely refused to come down and currently sits pretty high around 20 after the bearish Friday price action.

Chart: VIX Index (tradingView)

We’ll get more color on inflation this upcoming week with Tuesday’s PPI and Wednesday’s CPI release.

We also have the Fed's current economic conditions report via the “Beige Book” release Tuesday.

A strong economy and inflation pickup would be the bearish scenario for bonds. This would trickle into stocks and risk assets as a secondary effect.

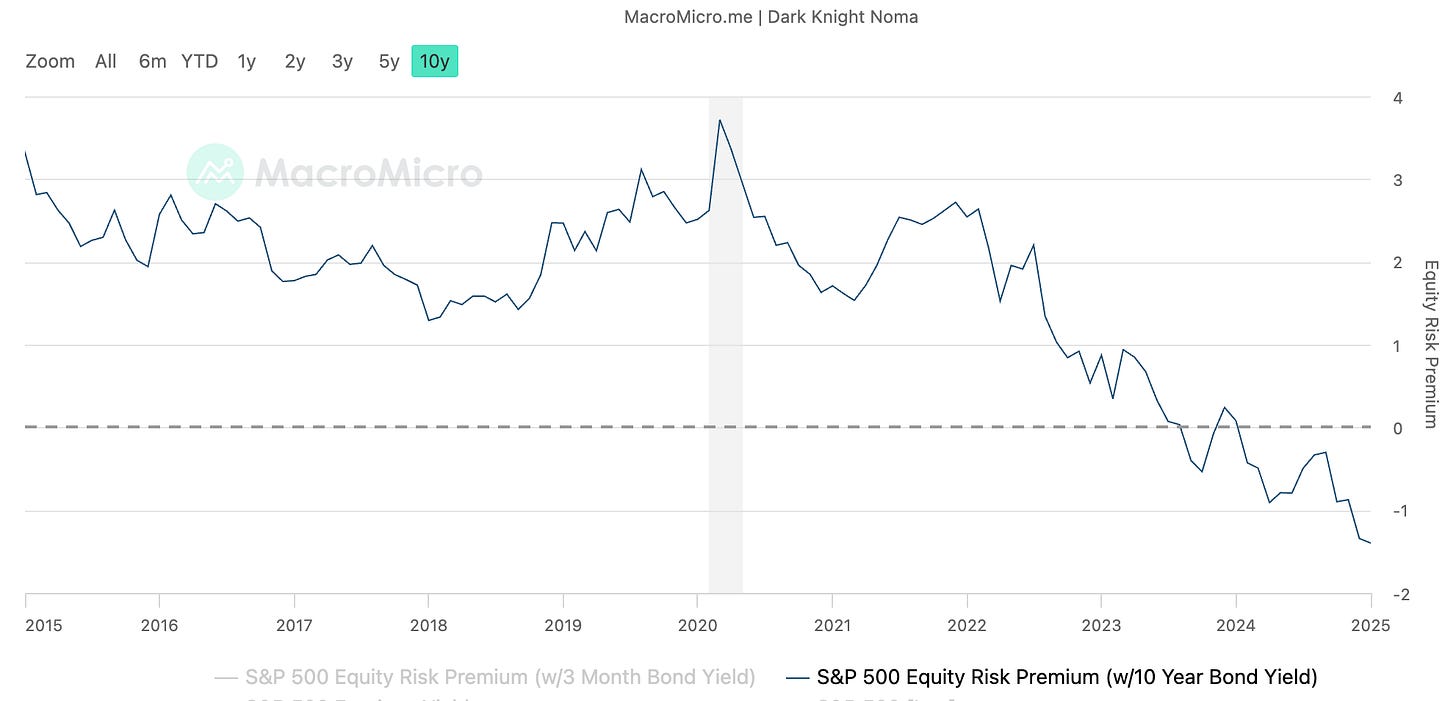

Keep in mind that the equity risk-premium (the additional return over risk-free bonds) remains historically low, which explains the bearish equity reaction as yields move higher, despite the strong economy.

Chart: Equity Risk Premium (macromicro.me)

BTC: $93,949 (-4.8% / 7-day)

ETH :$3,243 (-11.1% / 7-day)

SOL :$187.75 (-12.4% / 7-day)

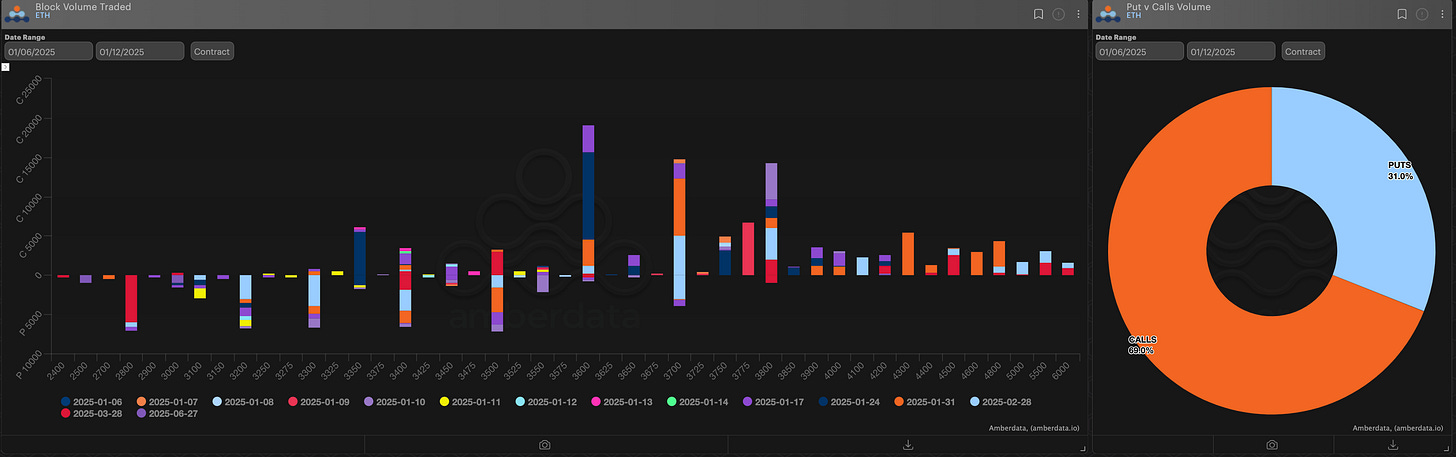

Crypto Options Overview

The market is getting a bit of mixed signals in terms of where Bitcoin goes from here in the short-term.

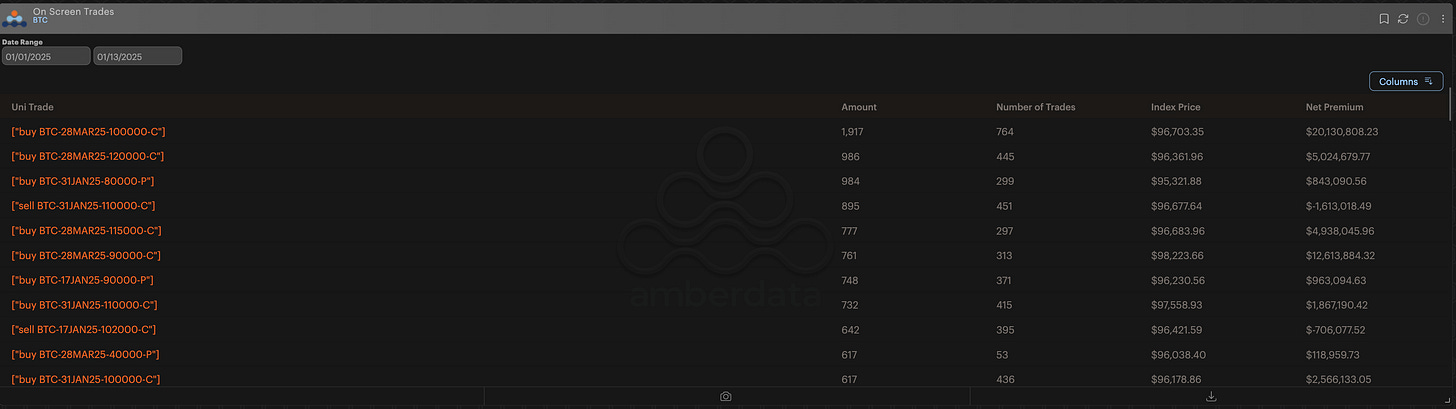

$100k remains a significant level and looking at on-screen “flows” both March $100k Calls and March $120k calls remain the most traded options from on-screen Deribit traders.

YTD on-screen traders are net “buyers” of these bullish calls.

That said, there are a few things to keep in mind.

On the one hand, the Trump inauguration, US and international BTC strategic reserves, new SEC regulations, and corporate treasury Bitcoin allocations are insanely bullish for the market.

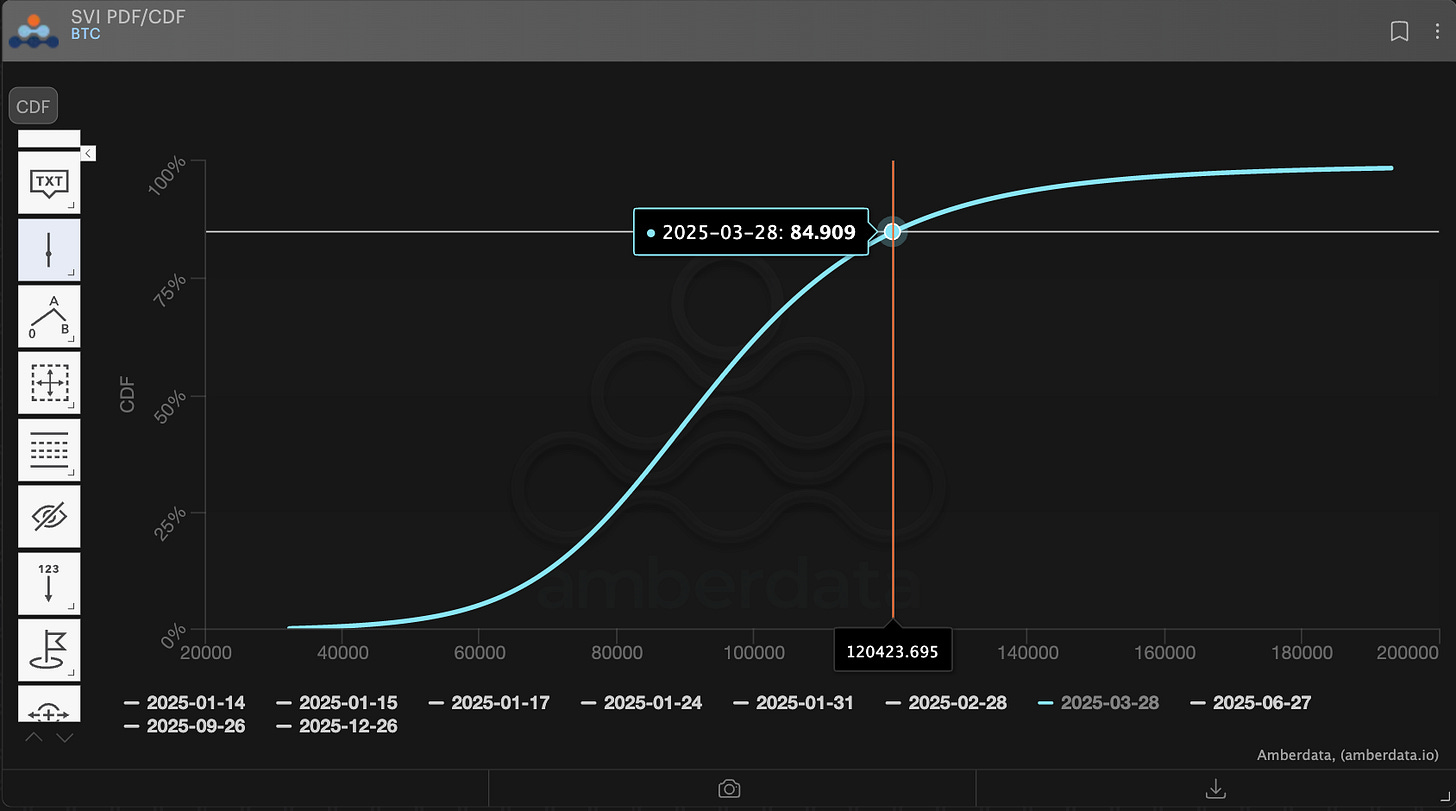

Given all this news, March expiration options only imply a 15% probability density ABOVE $120k which seems low should any of the above news headlines hit the wires.

On the other hand, higher bond yields, a weak stock market, and a potentially crowded crypto market (already positioned for everything mentioned above) mean prices might already include a lot of these bullish assumptions.

The battle of narratives might end-up giving us a breathing period of consolidation instead.

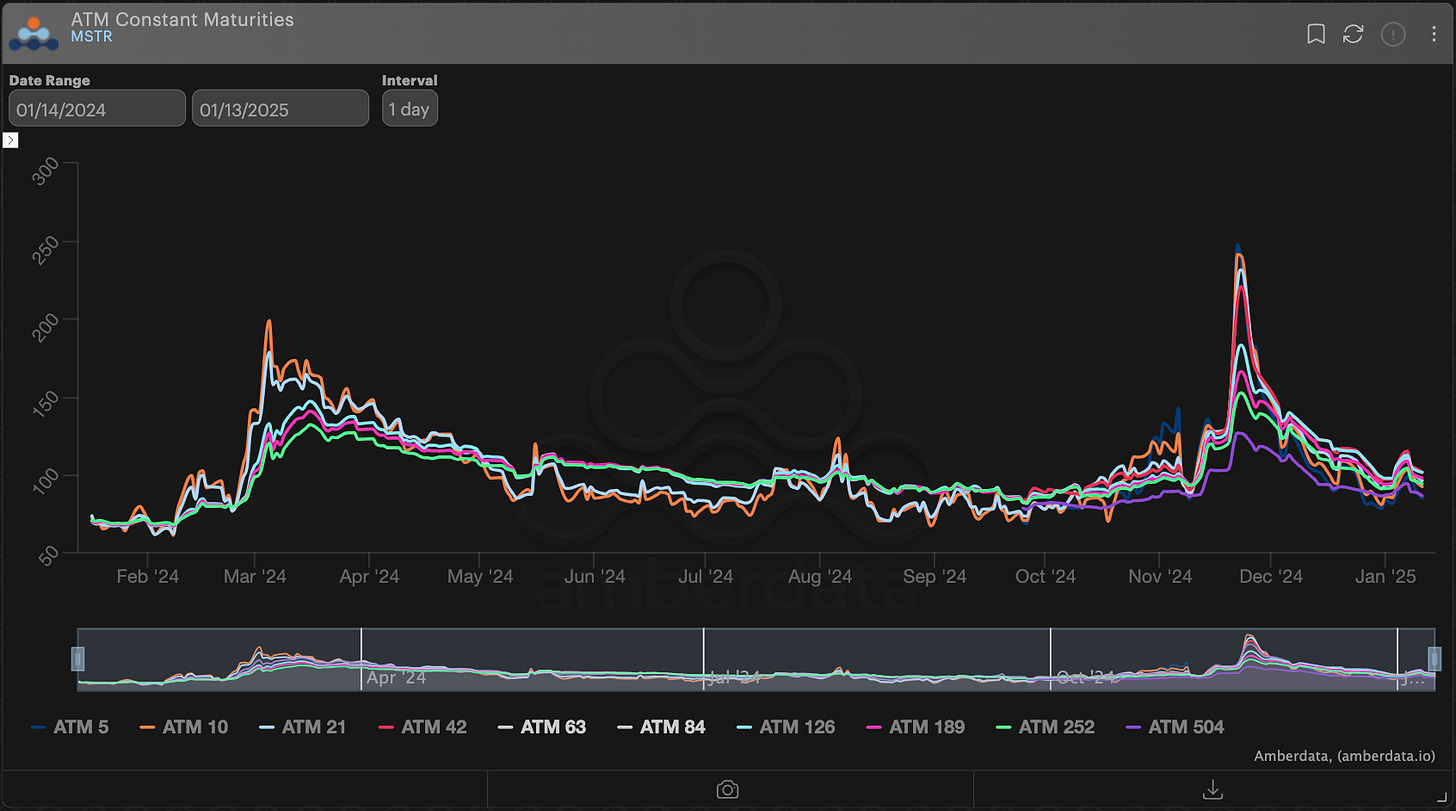

Looking at MSTR volatility, we can see that immediately after the election we had PEAK IV trading as high as 250% IV.

Today, we’ve nearly retraced the entire volatility pump to pre-election levels.

MSTR has now been added to the Nasdaq 100, MSTR has sold billions of convertible bonds to buy additional Bitcoin… what news is left to move the market?

Given this news, MSTR volatility might be a leading indicator for Bitcoin volatility.

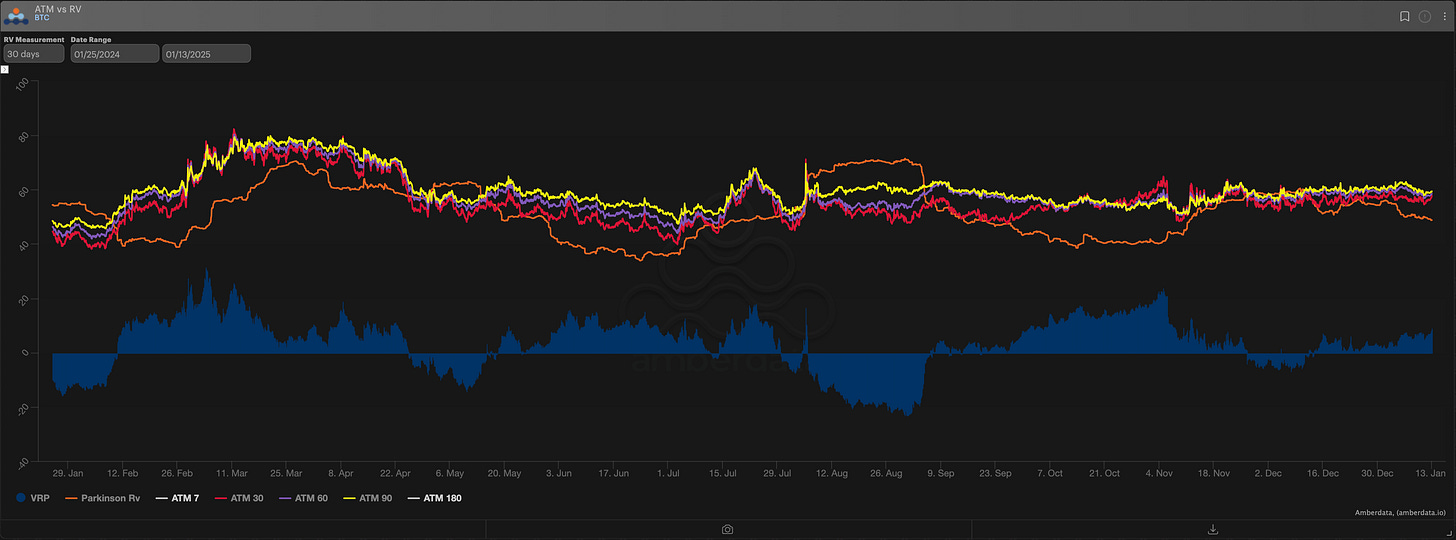

Bitcoin can remain spot bullish but a bit of calm in realized volatility could easily send implied back into the 40s. Notice the VRP already present in 30-dte.

Time decay and an implied volatility drop, could quickly devalue the $120k March calls sold at 62% IV.

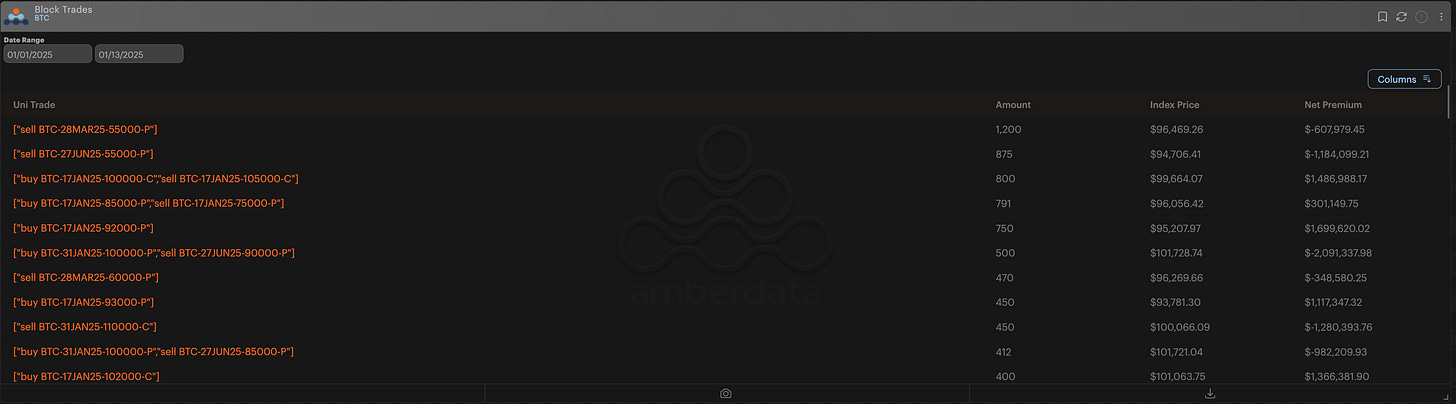

That’s something interesting to note, because when looking at top block trades, the institutional traders are also theoretically bullish on Bitcoin prices, but instead of buying calls, they’re selling March $55k Puts and June $55k Puts (shorting volatility rather than buying it).

An interesting distinction worth noting.

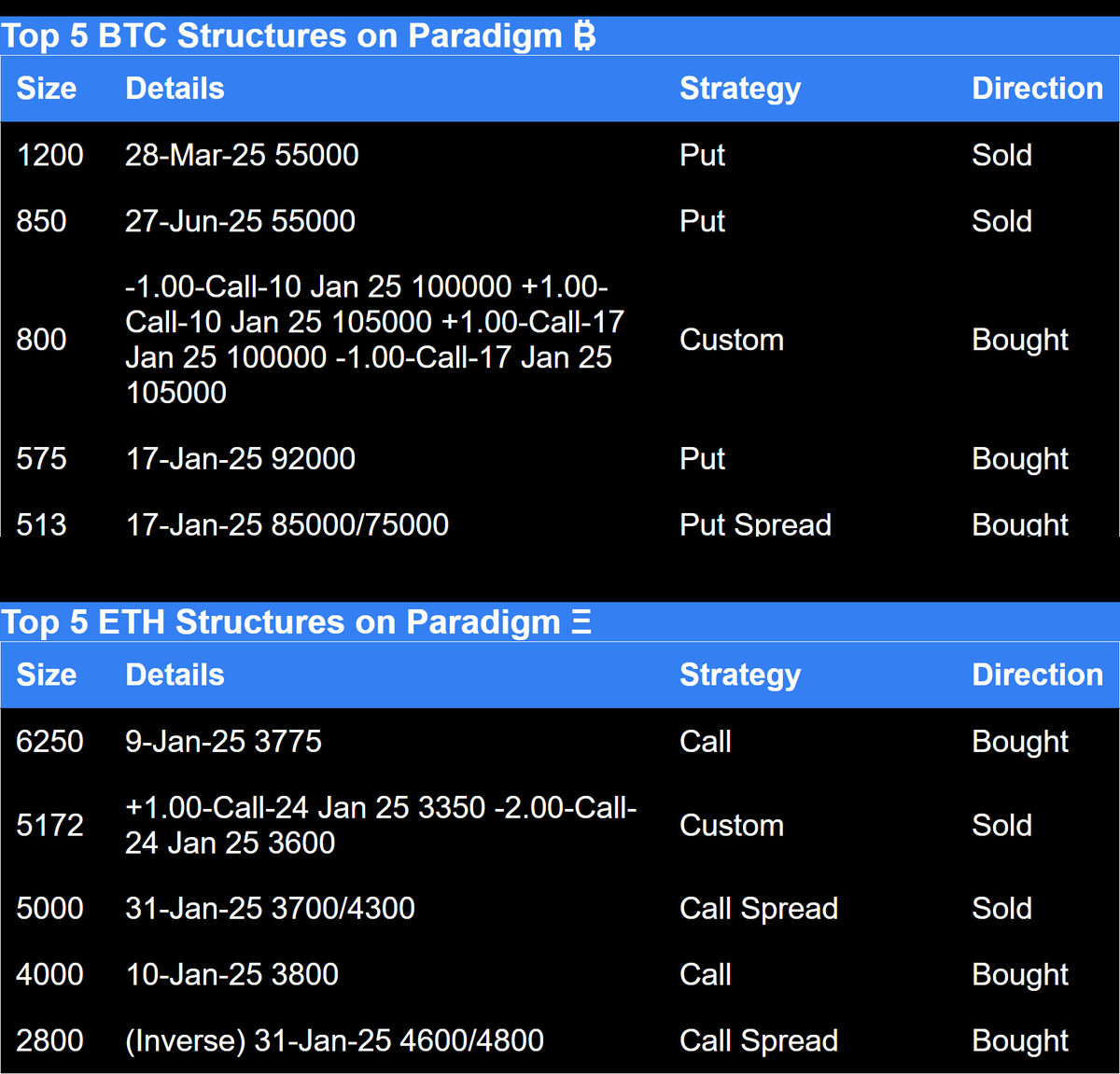

Paradigm's Week In Review

Paradigm Top Trades This Week

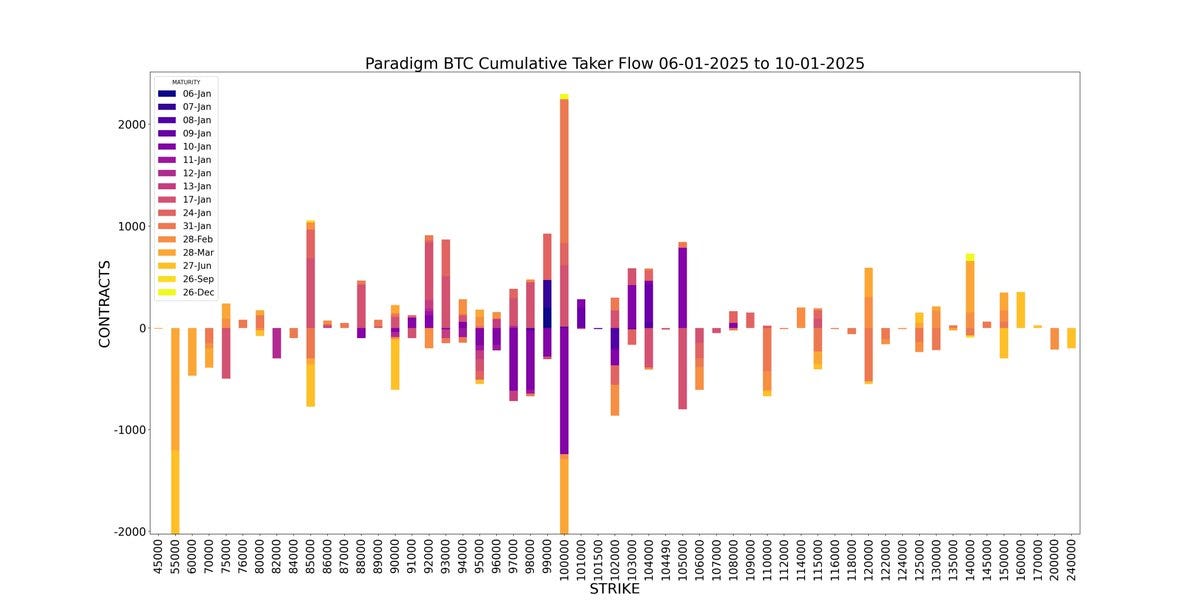

Weekly BTC Cumulative Taker Flow

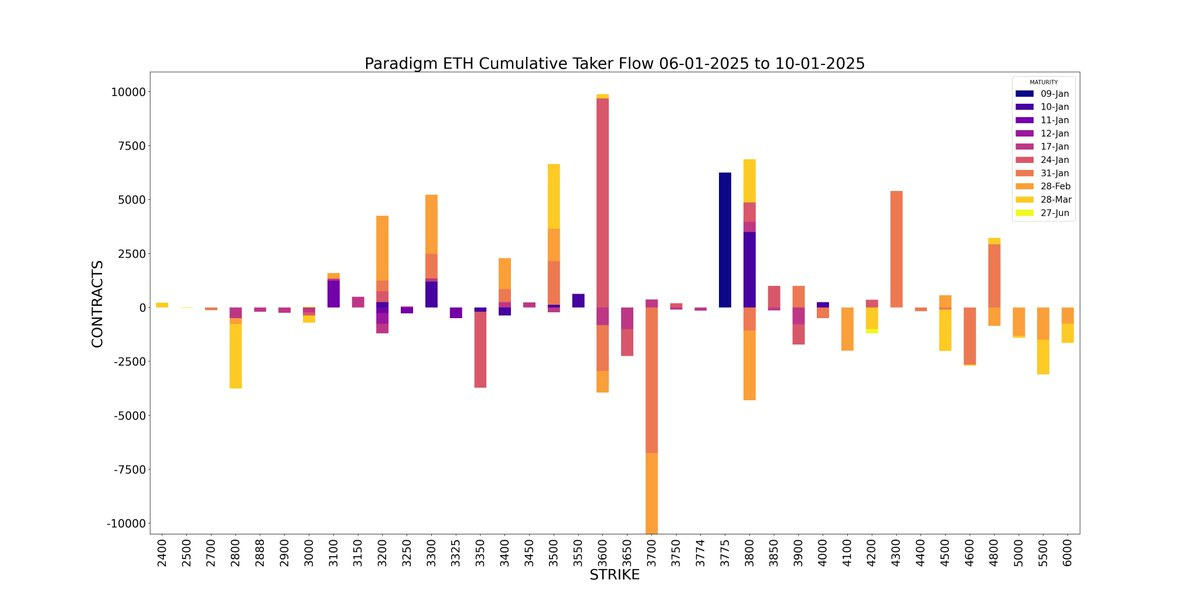

ETH Cumulative Taker Flow

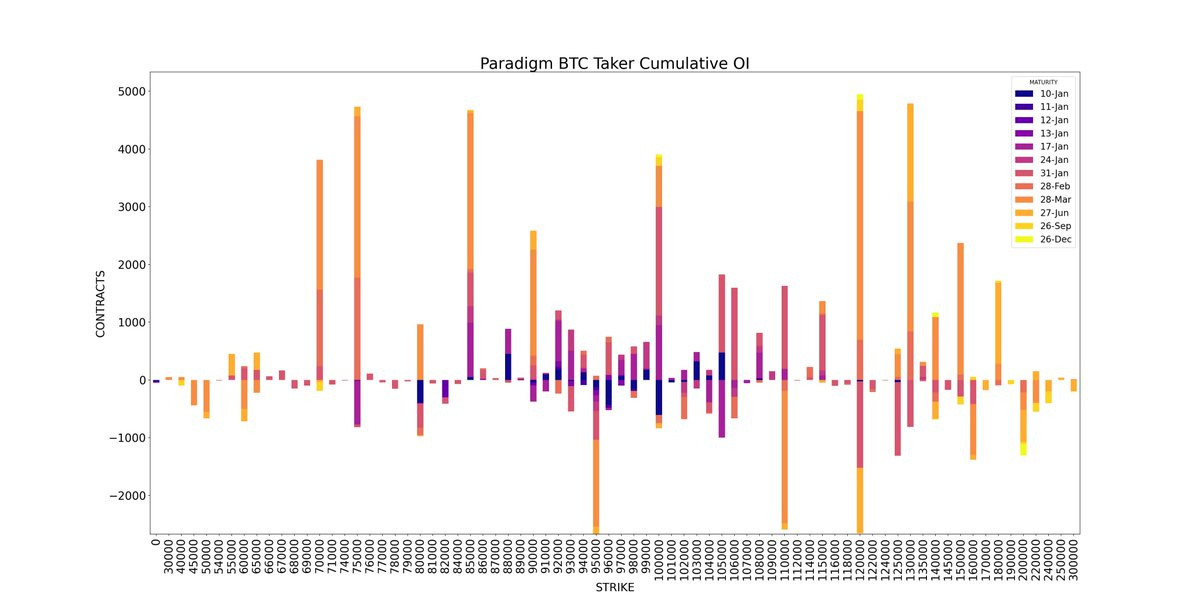

BTC Cumulative OI

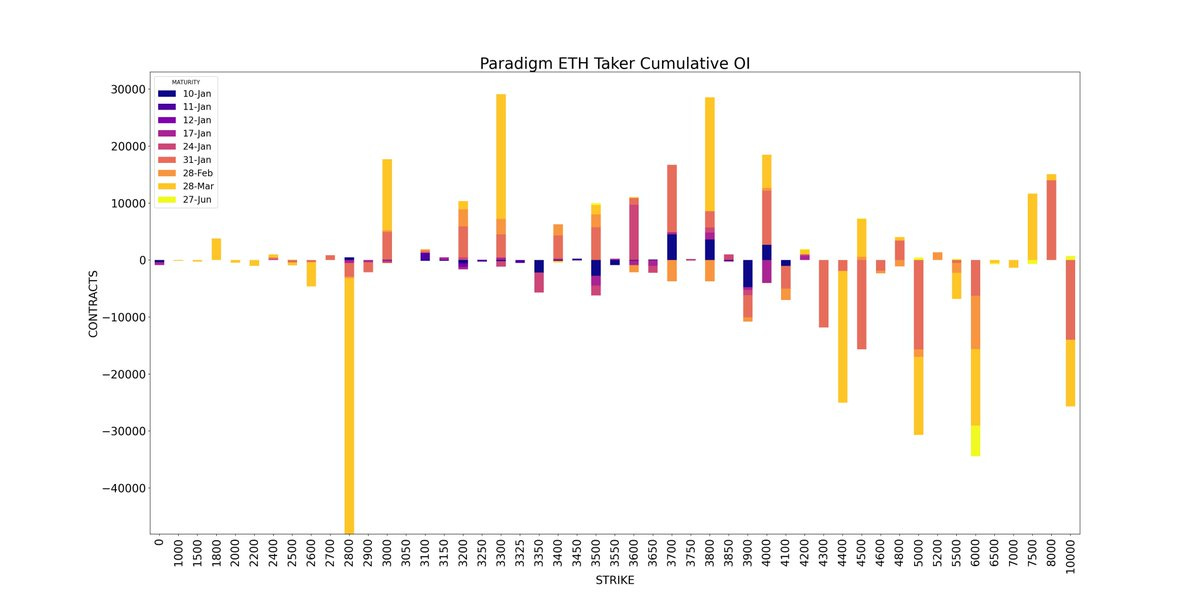

ETH Cumulative OI

BTC

ETH

- Derive’s token launch to go live Jan 15, 2025

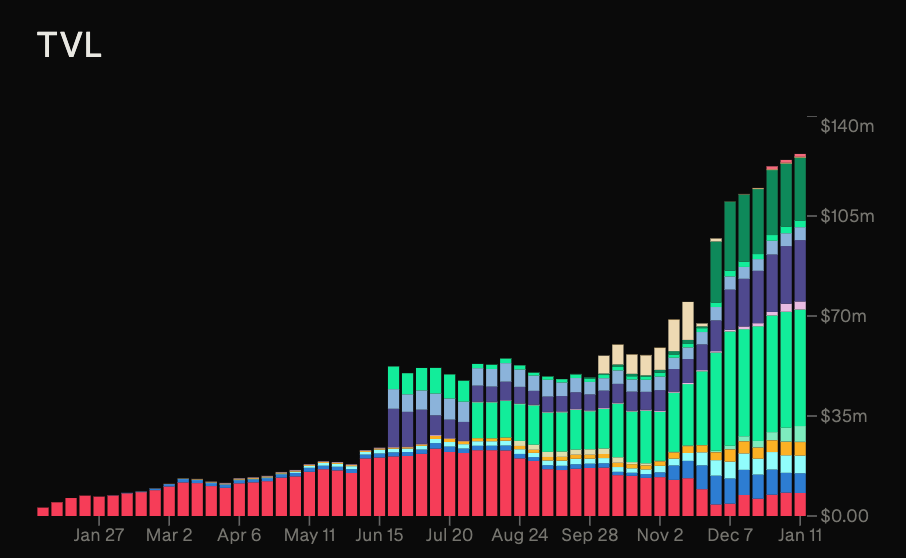

- TVL reaches new ATH of $128.6m

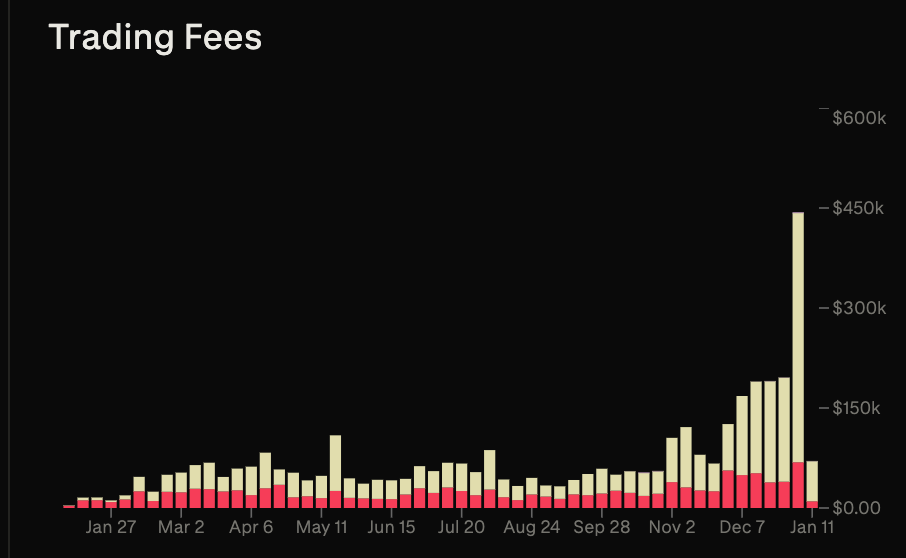

- Last week also a new ATH for weekly fees of $443K

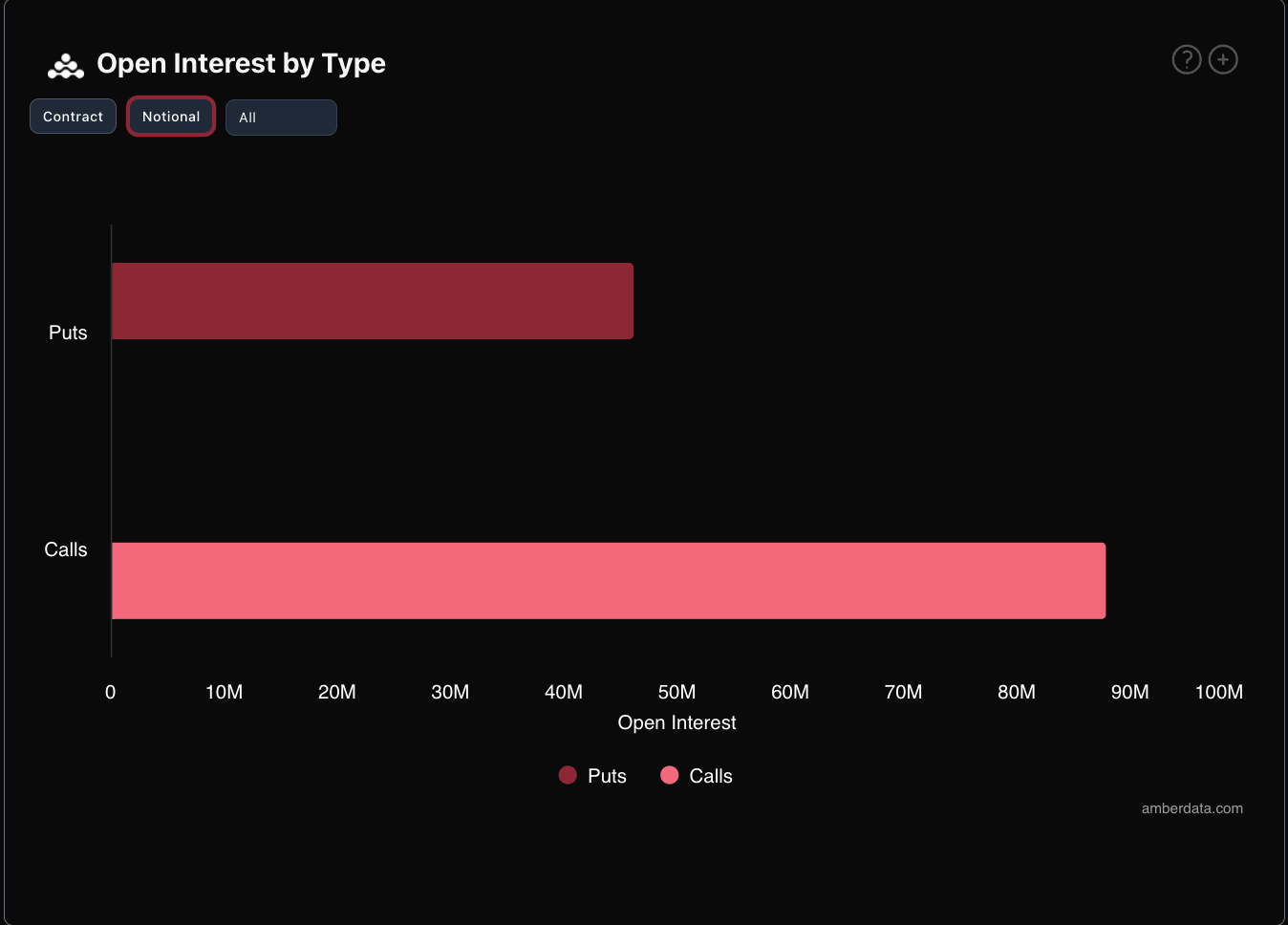

- BTC market is seeming more bearish as the percentage of put OI increased from just over 20% to nearly 35%.

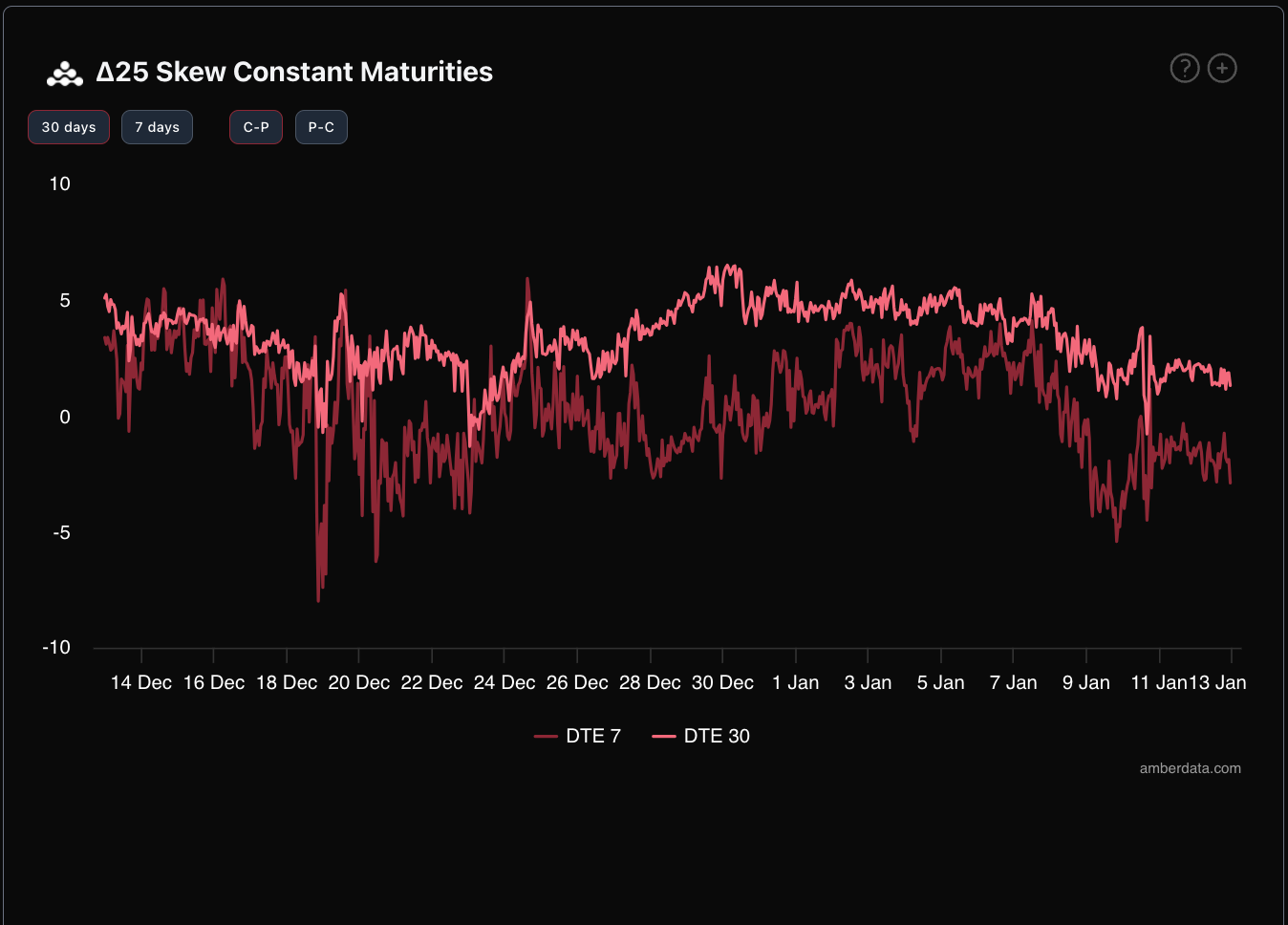

- 7 and 30 day ATM BTC IV both hovering near 55% while 25 delta skew have slowly fallen to -3% and 1.3% respectively.

- Derive markets are also the lowest place to borrow USDC against a swathe of collateral (borrow rate currently 3.14%).

AMBERDATA DISCLAIMER: The information provided in this research is for educational purposes only and is not investment or financial advice. Please do your own research before making any investment decisions. None of the information in this report constitutes, or should be relied on as a suggestion, offer, or other solicitation to engage in, or refrain from engaging, in any purchase, sale, or any other investment-related activity. Cryptocurrency investments are volatile and high risk in nature. Don't invest more than what you can afford to lose.